A raft of disappointing data this week coincided with warnings from the International Monetary Fund that South Africa must institute urgent structural reforms to address persistent weaknesses in the economy.

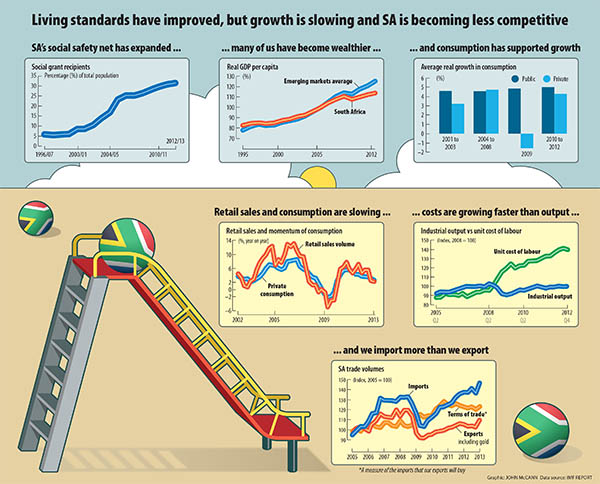

Among the numbers perhaps the most worrying was the trade deficit, which rose to over R19-billion as exports decreased by 7.6% for August and imports decreased by a mere 0.1%. The cumulative deficit was R107.31-billion compared with R69.91-billion in 2012, representing a 53% increase.

Labour disruptions were the likely cause for the slump in exports and continuing disruptions will "keep exports weak, with the impact of the strike in the automotive industry … likely to be visible in the coming months", Nedbank economists Isaac Matshego and Dennis Dykes said in a note.

There was still no clear indication that a weaker rand had worked to improve the country's trade balance, according to Stanlib economist Kevin Lings.

The slump in the trade figures will likely raise concerns regarding the perennial deficit on South Africa's current account — a measure of our trade in goods and services with the rest of the world.

It widened to 6.5% in the second quarter of the year and its funding is reliant on foreign capital inflows.

Confidence weakens

Confidence in the manufacturing sector also weakened this week, with the Kagiso Purchasing Managers Index declining to 49.1, the first fall below the 50 point mark since March, according to the Bureau for Economic Research.

Once again, industrial action, notably in the automotive sector, was cited as a reason for decline.

Although the effects of the strike action were likely to be temporary it did not detract "from the patchy nature of underlying growth in the sector", according to banking and asset management group Investec.

Consumer confidence had fallen to a decade low in the third quarter of this year and this, combined with a slowdown in the uptake of credit, should translate into a weakening in domestic demand, it said.

Business confidence was suppressed, which did not signal "a meaningful and sustained expansion of activity", Investec said.

Vehicle sales also fell this week thanks to supply disruptions and were likely to remain modest as poor consumer confidence off the back of a gloomy domestic outlook took its toll, Nedbank noted.

IMF's warning

The numbers coincided with the IMF's release of its annual country report on South Africa.

It warned that urgent structural reforms were needed to address low growth and widespread unemployment and inequality.

Growth had been hampered by international developments but domestic challenges including policy uncertainty that hampered investment and labour unrest played a role, said the IMF.

The reversal of capital inflows remained a risk to economic growth — which the IMF forecast at 2% for 2013 — given the country's twin budget and current account deficits.

This could be triggered by global factors — such as the "global repricing of risk" as advanced economies unwound unconventional monetary policies — or domestic ones, such as more labour and social unrest.

Implementing reforms outlined in the National Development Plan was "imperative to achieve faster growth and job creation".

Reforms to the labour market

The IMF warned that "parts of the tripartite alliance have opposed the plan which, together with the implementation record of structural reforms, leaves many investors sceptical about prospects for major structural change".

It recommended reforms to the labour market to increase flexibility and to the product markets to increase competition among dominant firms.

The IMF also recommended that the government adopt a debt benchmark to "bolster credibility" over its commitment to fiscal consolidation and the reduction in its deficit.

It also noted that while the rand's flexibility had helped the country absorb shocks, the building up of currency reserves would "help manage vulnerabilities".

In response to the report, the treasury said that the issues raised by the IMF report "are indeed issues that are already captured in government policies and programmes.

"The August Cabinet lekgotla agreed that the focus of the government, business and labour must be on accelerated implementation of domestic plans to grow the economy," the treasury said.

Blaming wage demands

However, trade union federation Cosatu panned the report and its endorsement of the National Development Plan, calling the IMF a "rabidly pro-capitalist, neoliberal organisation".

The report laid the blame for the poorly performing economy on rising wage demands and increases, Cosatu said, and was at odds with research done by the International Labour Organisation, which argued in favour of a wage-led growth strategy.

Cosatu said the National Development Plan fails to "fundamentally transform the structure of the economy, take forward the promotion of a new growth path to industrialise the economy, place job creation at the centre of the country's economic policy, and make redistribution and the combating of inequality and poverty a pillar of economic development".

?

?