Finance Minister Enoch Godongwana. (Photo: Mlungisi Louw/Gallo Images)

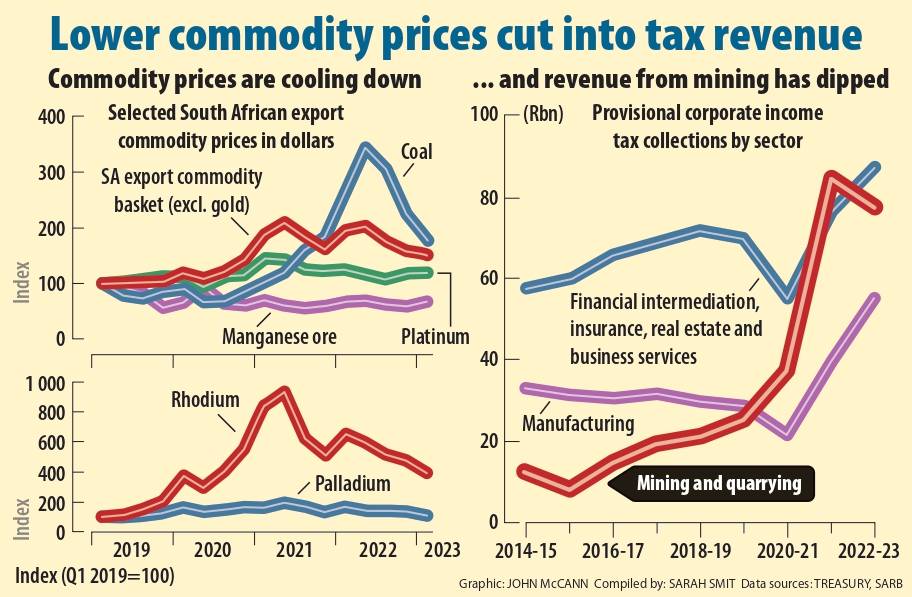

In the past month, a number of mining houses have reported significant declines in their profits, suggesting the country has seen the back of the economy-buoying commodity price boom.

Reports of lower mining profits come as Finance Minister Enoch Godongwana prepares to deliver his medium-term budget in about two months’ time. The mini-budget will give an indication of whether South Africa will be able to continue reining in its shortfall and bring some stability to the public purse.

But, with the economy skating on thin ice, South Africa’s fiscal outlook has deteriorated since Godongwana last gave an update on the country’s finances. The drop-off in mining sector profits indicate that another risk to the fiscus has reared its head.

Windfall

In his 2019 medium-term budget speech, then finance minister Tito Mboweni warned that sluggish global economic growth would hamstring South Africa’s recovery from the 2018 technical recession.

At the time, the world economy’s growth forecast was the lowest since the global financial crisis and commodity prices endured sharp declines. With spending continuing to outpace revenue, South Africa’s budget shortfall would end up being the country’s biggest since 2009. After the pandemic hit — which caused the deficit to widen to a record 10% of GDP — it became clear that the country’s fiscal outlook would get worse before it got better.

And it did get better.

In February 2023, after surging commodity prices buoyed tax revenues, the treasury (led by Godongwana) declared it would in the 2022-23 fiscal year achieve a primary surplus — when revenue exceeds non-interest spending — for the first time since 2009. This was as the mining windfall pushed revenue collections R93.7 billion above the 2022 budget forecast.

The primary surplus ought to have marked the end of a painful period of fiscal consolidation.

The treasury said that in 2023-24, the budget deficit will narrow to 3.9% of GDP — the lowest since 2019. South Africa would achieve successively larger primary surpluses in the medium term (0.9% in 2023-24, 1.2% in 2024-25 and 1.7% in 2025-26), according to the forecasts contained in the 2023 budget.

Back to reality

But analysts were sceptical that the government would be able to extend the fiscal winning streak given lingering spending pressures and the country’s dismal track record for delivering economic growth.

Since Godongwana’s tabling of the 2023-24 budget, the economic outlook has deteriorated significantly, largely as a result of load-shedding.

In February, the treasury forecast that the economy would grow 0.9% in 2023, 1.5% in 2024 and 1.8% in 2025. More recently, the South African Reserve Bank forecast growth of 0.4% in 2023, 1% in 2024 and 1.8% in 2025.

Low growth and additional spending have caused some to come up with far less optimistic fiscal projections. Absa economists, for example, don’t see the government achieving a primary surplus until 2026-27. They also forecast a revenue shortfall of R39 billion compared with the 2023 budget target.

Unbudgeted spending pressures abound, the Absa economists noted in their most recent quarterly outlook. These include a R2.4 billion bailout for the South African Post Office, a possibly expanded social relief of distress grant and the eventual implementation of the National Health Insurance.

A report by the University of the Witwatersrand’s Public Economy Project (PEP), released in June, noted that, although the government did manage to achieve a small primary surplus in 2022, this does not hold up against more realistic assumptions. The PEP — which contends that South Africa faces permanent austerity, which is steadily eroding the state — forecasts primary deficits for 2023, 2024 and 2025. The main budget deficit, according to the PEP’s expectations, will continue to worsen over the medium term — nearing the 2019 figure.

Commodity cliff

The PEP report notes that the unanticipated wave of inflation, experienced in the latter half of 2021 and in 2022, aided the government’s consolidation efforts by raising the nominal GDP growth, increasing the tax take and cutting back on the real growth of spending. “This buoyancy partly reflected the commodity price boom that followed the pandemic,” the report added.

A 2022 Reserve Bank paper also points to the implications of the commodity boom on the public purse, noting that the higher prices almost fully offset the negative effects of lower production and consumption in the real economy. “If the revenue boost from the terms of trade unwinds before other private sector spending and growth have increased (and the output gap has closed), fiscal deficits will increase sharply,” the paper adds.

Recent shareholder updates from mining companies suggest the commodity windfall has slowed significantly. This week Northam Platinum projected an up to 12.5% fall in headline earnings per share compared with the 2022 financial year. Although the platinum miner reported increased production, it noted that adverse market developments have caused a material contraction in profit margins and cash generation capacity across the platinum group metals (PGM) industry.

The PGM industry received a boost in the aftermath of the pandemic, after outpacing coal sales for the first time in a decade, but prices started to decline in 2022. But South Africa’s commodity basket received a second wind in 2022, when Russia’s invasion of Ukraine inflicted further supply constraints.

One big winner of the Russia-Ukraine fallout was the country’s coal-mining industry, which saw prices soar amid increased demand from energy-strapped Europe.

Last week, major coal mining companies Glencore and Exxaro announced that their profits plummeted in the first half of 2023.

In Glencore’s case, earnings before interest, taxes, depreciation and amortisation were down 50% on 2022, according to the company’s 2023 half-year report. Glencore attributed this earnings fall to the normalisation of energy market imbalances and volatility “from the extreme levels seen in 2022”.

Last month, when Anglo American Platinum and Kumba Iron Ore cautioned that profits in the six months ending June 2023 could fall by 75% and 22%, respectively, the Bureau for Economic Research (BER) said “a major local fiscal risk that we have cautioned about is materialising”.

“Surging mining profits were the mainstay of a corporate income tax bonanza in 2021 and to a lesser degree also in 2022,” the BER added.

“The abrupt change in fortunes places major downside risk on corporate, and overall, tax revenue in the current (2023-24) fiscal year. This is an important reason why, for some time, we have cautioned that treasury was set to vastly undershoot its February 2023 main budget deficit expectation (3.9% of GDP) for 2023-20.”

(John McCann/M&G)

(John McCann/M&G)

Ambitious

The market is pricing in a government revenue shortfall of R40 billion to R60 billion, according to Momentum Investments economist Sanisha Packirisamy. She noted that achieving a primary surplus will be an issue for the near to medium term as softer revenue and higher spending converge to dampen the fiscal outlook.

Stanlib chief economist Kevin Lings noted that commodity prices have softened and demand isn’t as robust as expected, partly the result of China’s less robust economic rebound. There was a distinct weakening in corporate tax revenue in June, he added. “It is not disastrous, but it does put us on track to collect less revenue than was budgeted.”

When asked whether the government used the commodity windfall appropriately, Lings noted that part of the added revenue went towards reducing debt and to consumption expenditure.

“Over time, the structure of the budget has overwhelmingly moved towards consumption and away from infrastructure. And that has been to our detriment … what would have made a bigger difference is if not all of the money went to debt reduction, but a portion [was] used to revitalise critical infrastructure,” Lings said, noting that many mining companies were unable to fully cash into the commodity boom because of logistical constraints.

Lings said the main budget deficit will probably be closer to 5% of GDP, instead of the 3.9% treasury forecast.

“It’s very clear that, without strong economic growth, it is very difficult to effect fiscal discipline, because you just have this constant demand to spend money,” he added, noting that revisions to the treasury’s fiscal projections come October are likely.