Forner ITB chairperson Jerome Ngwenya. Photo: Supplied

The Zulu monarchy appears to have been the target of a complicated scam in which it was promised investments totalling $2 billion (R36 billion) for community development projects on land under the Ingonyama Trust’s control.

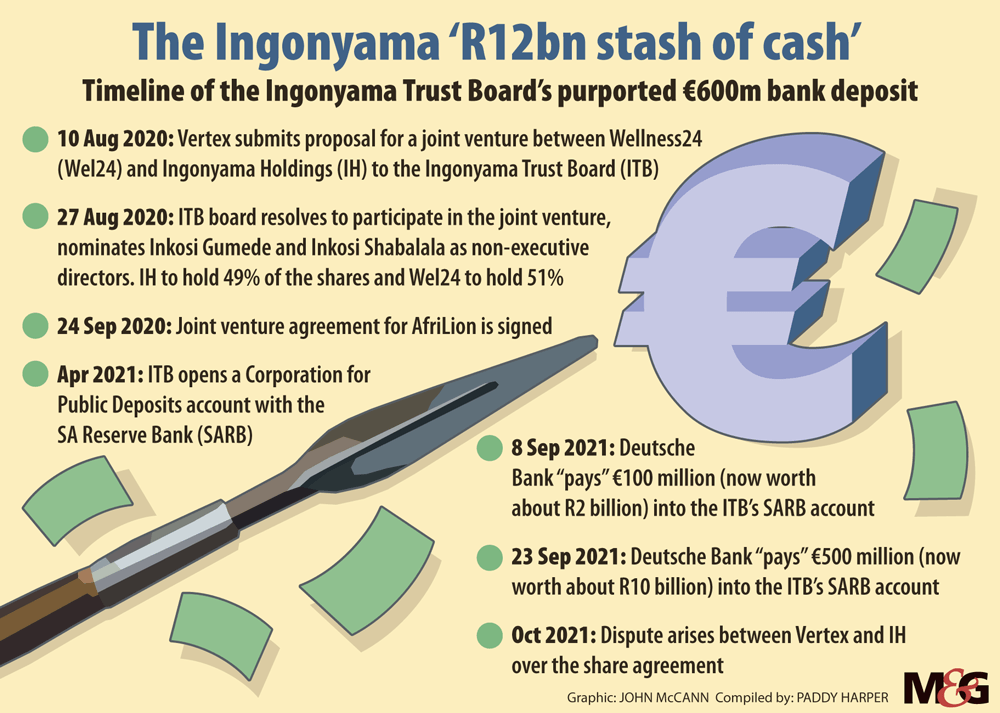

Ingonyama Trust Board (ITB), set up in the early 1990s with then Zulu king Goodwill Zwelithini ka Bhekuzulu as its sole trustee, went as far as opening an account with the South African Reserve Bank to facilitate receiving funds from abroad and signed a memorandum of understanding with Vertex Global Holdings to set up a joint venture, AfriLion.

Although initial transfers totalling R12 billion (€600 million) were purported to have been paid into the Ingonyama Trust Board’s bank account 18 months ago by European investors for the joint venture, sources close to the matter said that did not happen.

The money was alleged to have been paid in two tranches of €100 million and €500 million to the ITB’s account with the Reserve Bank on 8 September 2021 and 23 September 2021, respectively.

The Ingonyama Trust Board administers nearly three million hectares of KwaZulu-Natal on the king’s behalf and collects revenue from commercial tenants running businesses and mines on land it controls.

According to documents leaked to the Mail & Guardian, the funds, secured from an international investor, were moved from controversial Swiss bank Julius Baer & Co — nailed in 2021 for laundering bribes paid to Fifa officials — into the ITB’s account through Deutsche Bank AG in Frankfurt.

The “money” was destined for use by AfriLion, a joint venture between Ingonyama Holdings, the ITB’s investment wing, and Wellness Holdings, a subsidiary of Vertex Global Holdings, which was founded by cannabis entrepreneur Gerhard Naude.

Although Naude had initially contacted the late Zulu monarch, Goodwill Zwelithini ka Bhekuzulu, on commercial cannabis farming before his death, the project was modified to focus on Covid-19 relief measures for people living on land under the ITB’s control.

But, according to correspondence seen by the M&G, a dispute arose between the ITB and Naude over the memorandum of understanding between the two entities, which gave Ingonyama Holdings 49% of AfriLion and Wel24 (the trading name of Wellness Holdings) 51%.

The correspondence shows that ITB chairperson Jerome Ngwenya expressed concerns that the structure of the agreement might not comply with the Public Finance Management Act (PFMA) and be “viewed as money laundering”. He raised the concerns days after the first “payment” was “received” — and 12 months after the agreement was signed between Ingonyama Holdings and Wel24.

Ngwenya is understood to have subsequently met Naude to try to resolve the impasse between the two entities during 2021, but failed to reach an agreement over the memorandum, effectively ending their relationship.

The latest disclosure about the ITB’s financial dealings comes at a time when new Zulu king, Misuzulu ka Zwelithini, has intervened in the running of the entity, of which he is the sole trustee, instructing Ngwenya to make its finances and programme public.

(John McCann/M&G)

(John McCann/M&G)

The monarch did so days after the M&G exposed the ITB’s failure to account to the Auditor General of South Africa (AGSA) for R41 million paid to lawyers and a four-month-old investment company for joint projects with Ingonyama Holdings.

Ingonyama Holdings was set up in November 2019 with Ngwenya and former ITB chief executive Lucas Mkhwanazi as directors. It began an investment drive, using R41 million from the Ingonyama Trust to fund its operations and to pay for joint ventures with AIN Capital, which was founded in November 2020, four months before it received the first payments from the ITB.

The AIN transactions — and the Vertex/AfriLion deal — were red flagged by whistleblowers in the ITB at the time. Board member Linda Zama resigned rather than be associated with the AIN deal, which was also opposed by the ITB’s deputy chairperson, Zethu Qunta, who has also since resigned.

Lawyer Jaco Loots, of Phosa Loots Attorneys, said the firm had been asked to facilitate the transaction, but that it had not taken place.

“We were approached to facilitate the transaction right in the beginning as we have experience in that area. Unfortunately it was not successful, ” Loots said. “Our involvement in the matter ended there.”

Naude declined to comment or to name the investor from whom the money had been received, saying it came from a private equity fund managed by Julius Baer & Co. He was, however, adamant that the money had been transferred to the Reserve Bank.

Naude is the founder and former chief executive of Go Life International, a wellness company listed in Mauritius and on the JSE.

He is involved in a legal battle with Go Life, which in 2020 issued a warning through a shareholder letter against him and former director Eugene Alt for allegedly “misrepresenting” themselves as being part of Go Life and of attempting to force their way into its projects.

In 2021, Naude told the M&G he had raised the first tranche of $2 billion from foreign investors for the AfriLion project, which would focus on healthcare, property development and construction, mining and energy and commercial cannabis.

“We are planning for a few projects to kick off in the first quarter of 2022. As a group we will not only focus on KwaZulu-Natal, but also on the rest of Africa. We have already engaged with communities, where we will focus on creating jobs and uplifting the lives of all the people staying in those communities,” he said at the time.

The decision to enter the joint venture was taken by the ITB in August 2020, based on a five-page proposal submitted by Naude for projects focusing on Covid-19, with further funding to be made available for “health-related projects, employment creation (infrastructure development) and other humanitarian purposes”.

The ITB agreed to set up the joint venture, appointing inkosi Zwelinzima Gumede and inkosi Siphiwe Shabalala as non-executive directors, and to open the Reserve Bank account to facilitate the transaction.

A memorandum of joint venture agreement for the new company was signed by Mkhwanazi and Naude on 30 September 2020, but was later rejected by the ITB, days after the first €100 million was purported to have been paid.

(John McCann/M&G)

(John McCann/M&G)

According to documentation seen by M&G, the €100 million was “paid” into the ITB account from Julius Baer & Co through Deutsche Bank AG in Frankfurt on 8 October 2021. The second payment was purported to have followed the same route two weeks later.

Julius Baer & Co is itself no stranger to controversy.

In May 2021, the Swiss bank paid $80 million in fines to the United States justice department in a deferred prosecution agreement over $36 million in bribes paid to Fifa officials for broadcast rights. Last November, its UK subsidiary, Julius Baer International, was fined $21 million for paying bribes for business from the now defunct Russian oil company, Yukos.

Correspondence between Ngwenya and Naude on 16 October 2021 reveals that both parties were concerned that the funds needed to be “moved” to avoid being diverted to “ghost accounts”.

Ngwenya expressed concerns about the memorandum of understanding between Ingonyama Holdings and Wellness and a revised version that had been drafted by Naude but had not yet been signed.

“I agree with you that there remains a huge risk if the funds do not move. Ghost accounts have become the order of the day. However, as the agreement stands I have few issues to raise,” he wrote. “In short, the agreement should also be PFMA compliant. As it stands it leaves a huge loophole for the IT account being viewed as [a] money laundering account, rightly or wrongly.”

Ngwenya said he was studying the agreement “in great details” and was also referring it to the ITB’s lawyers “to have an independent view on it” and asked that Naude meet him to resolve “tension” with Mkhwanazi.

Ngwenya said that a term sheet — a non-binding agreement outlining terms for a potential business deal — had already been received from Richards Bay Minerals, which mines on ITB land, and that another from Credit Suisse was “on its way”.

“We must take a long term view on the relationship. You are the

first to confirm that the amount at stake right now is very small compared to what is as yet to come. You have demonstrated in a short space of time your credibility,” Ngwenya said.

“We owe it to you and the brand Ingonyama to play open cards and complete transparency. I once more request of you to indicate your availability.

“The last thing I wish to see is a delay in the release of these funds and the implementation of the necessary projects and gaining public confidence, especially Ingonyama Trust beneficiaries.”

It is understood that at the subsequent meeting, negotiations broke down, with Ngwenya refusing to allow the ITB to act as a “paymaster” for the projects without having full control over the funds.

Ngwenya had not responded to messages, emails and calls from the M&G at the time of writing.

A spokesperson for the Reserve Bank said it was unable to provide information on the matter because its relationship with its clients was confidential.