Fuel prices have also fallen this month, which might have helped keep inflation in check, although it remains to be seen what effect the rand’s weakness will have had. (Dwayne Senior/Bloomberg via Getty Images)

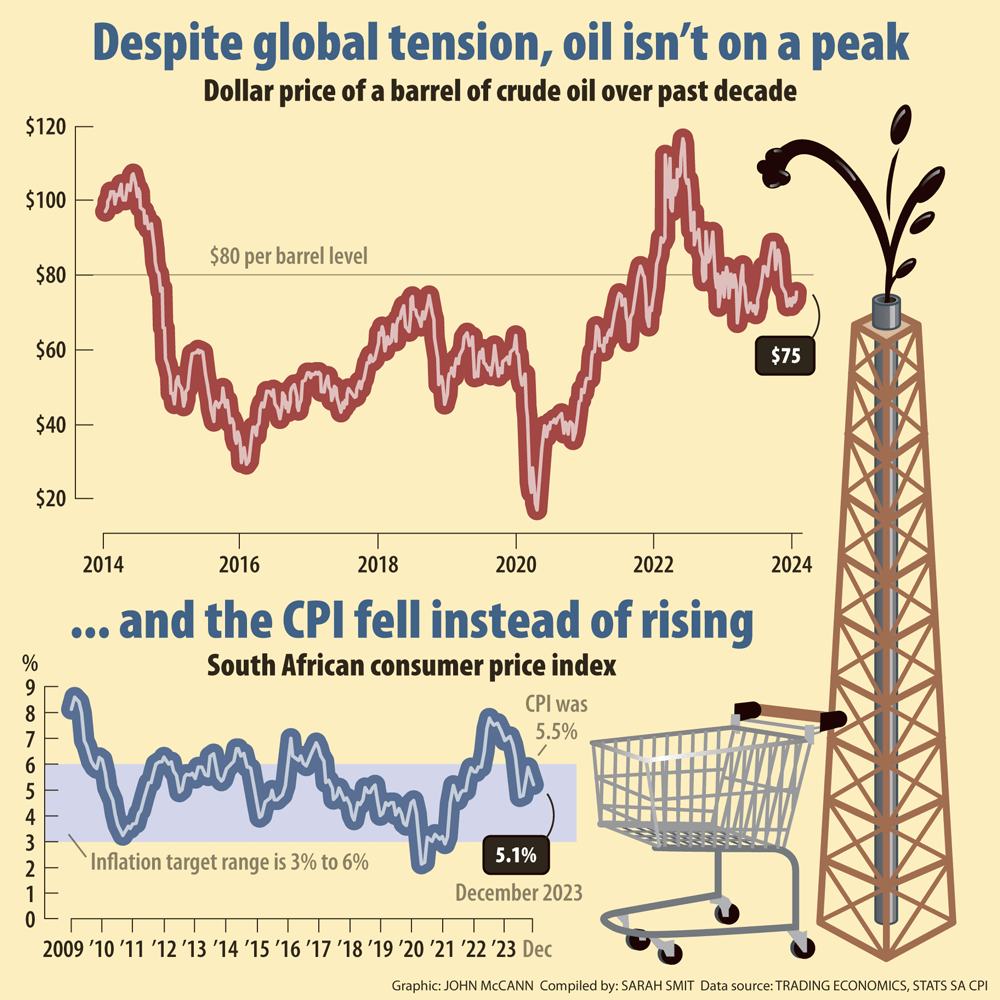

Despite growing tension in the Middle East, as well as Eastern Europe, oil prices have held below $80 per barrel during the first weeks of the year.

Insofar as inflation is concerned, the fact that prices haven’t surged to the heights that they did during the first year of Russia’s invasion of Ukraine is good news. However, the response by oil markets to recent geopolitical shocks suggests trouble is brewing on another front.

Data from Statistics South Africa this week showed domestic inflation eased to 5.1% year-on-year last month, partly off the back of lower fuel costs.

That month, motorists were afforded some relief when petrol prices decreased by 65 cents a litre. Diesel prices fell even more sharply, by between R2.35 and R2.41 a litre.

Fuel prices have also fallen this month, which might have helped keep inflation in check, although it remains to be seen what effect the rand’s weakness will have had.

The decline in oil prices has come about despite the escalating geopolitical friction in two major oil-producing regions.

Indeed, Israel initiated its siege on Gaza, a number of analysts warned that, should the conflict spill out into other parts of the Middle East, the world could see a repeat of the oil price spiral that occurred when Russia first invaded Ukraine.

When Moscow’s assault started, oil prices shot up to over $100 a barrel and eventually reached the highest price in over a decade.

Prices eventually came down but remained somewhat volatile during the course of last year. While they rose in the immediate aftermath of Israel’s war, they ended up falling to their lowest level since 2018.

Since the bombardment of Gaza began in October, tension has spread to other parts of the region, notably in the escalating conflict in the Red Sea.

This week, the US and the UK launched a fresh round of airstrikes on Yemen. The strikes, the eighth in nearly two weeks, are in retaliation to the Iran-aligned Houthis, who continue to target vessels in the Red Sea — one of the world’s most densely packed commercial shipping routes.

The militant group, which controls parts of Yemen, has said its attacks are in response to Israel’s US-backed war on Gaza.

(Graphic: John McCann/M&G)

(Graphic: John McCann/M&G)

Explaining why oil prices haven’t soared the way they have done in the past, Razia Khan, chief economist and head of Middle East and Africa research at Standard Chartered, noted that, compared to other asset markets, oil markets have taken “a uniquely bearish view on the global economic outlook”.

Very little, if any, geopolitical risk premium is currently in the price, Khan added. “This poses risks if any expansion of the conflict actually disrupts global oil supply significantly. We’ve not seen this yet.”

Investors are weighing the crisis in the Middle East against questions over economic growth, which will affect global demand for oil.

When Russia first invaded Ukraine, the global economy was still in recovery mode from the Covid-19 pandemic — which caused global oil demand to contract for the first time since the 2009 recession. Oil companies enjoyed a considerable rebound in 2021, as demand shot up again.

However, the global economy looks a lot different to the beginning of 2022, when financial conditions were much more accommodative than they are today. Interest rate hikes, inflicted in the wake of Russia’s war, have weighed heavily on the global economy, which is in for another tough year.

The World Economic Forum’s Chief Economists Outlook, which was released last week, noted: “The relative resilience of the world economy in recent years will continue to be tested entering 2024. Global economic activity is stalling with signs of slowdown in both the manufacturing and services sectors.”

The report also flags the effect of geopolitical rifts on the health of the global economy.

Forecasts in the World Bank’s Global Economic Prospects report suggest that — despite easing inflation and the promise of interest rate cuts — global economic growth will slow this year, for the third consecutive year.

“The recent conflict in the Middle East has heightened geopolitical risks and raised uncertainty in commodity markets, with potential adverse implications for global growth,” according to the report.

“This comes while the world economy is continuing to cope with the lingering effects of the overlapping shocks of the past four years — the Covid-19 pandemic, the Russian Federation’s invasion of Ukraine and the rise in inflation and subsequent sharp tightening of global monetary conditions.”

Last week, the International Energy Agency said increases in global oil demand are set to halve from 2.3 million barrels a day last year to just 1.2 million barrels a day this year, pointing out that the post-pandemic recovery is all but complete and that GDP growth is below trend in major economies.