Financial Mail

Tax advisers at law firm ENSafrica sold tycoon Christo Wiese a lemon — one that now implicates him, ENS and Tullow Oil in an alleged multibillion-rand “tax evasion” scheme.

This emerges in court papers filed in the Western Cape High Court, in which the SA Revenue Service (Sars) claims that ENS created an aggressive tax structure to help Tullow shift assets worth R3.9bn out of SA, dodging taxes in the process.

Sars is now pursuing Wiese, a former ENS executive, and two other people personally for R217m, as part of a R3.7bn tax claim based on Tullow’s “restructuring ”. When contacted about this story, ENS tax head Peter Dachs denied that Sars alleges any tax evasion “in respect of the merits” of the long-running dispute.

ENS, which is due to move into a glitzy 17-storey office tower in Sandton next month, bills itself as Africa’s largest law firm, with 600 lawyers focused on doing “what’s best for the client”.

In this case, Sars claims ENS restructured Tullow, leaving it in charge of a holding company in SA that was little but a tax shell — which the law firm then sold to Wiese.

When Sars came knocking, Wiese allegedly moved assets out of the company and sold it to a former ENS executive who told Sars there was no cash or assets left to claim. The case is due to be heard in court next month.

This is more bad news for Wiese who, until last year, was SA’s wealthiest citizen by a country mile. However, the collapse of furniture retailer Steinhoff, which he chaired until December, caused Wiese’s wealth to tumble by R59bn. Wiese tells amaBhungane he got no tax benefit from the scheme.

However, it seems he tried to — but Sars stopped him. Tullow, which was started in Ireland in 1985 to exploit Africa’s forgotten oil fields, is valued at £3.2bn on the London Stock Exchange. It boasts that it is “Africa’s leading independent oil company”, based on its operation in 10 African countries. However, it has regularly found itself wrapped up in tax controversies.

In 2013, a nongovernmental organisation called Platform London claimed Tullow had created artificial structures to minimise its profit in the UK to avoid paying tax. “From 2011 to 2012, Tullow increased its pretax profits from $1.07bn to $1.1bn, but in the same period the rate of corporate tax that it claimed was due dropped from $37.4m to $10.1m,” it said.

Tullow has not responded to amaBhungane’s questions.

Normally, this isn’t the sort of dispute one reads about, as raw details of tax disputes are usually protected by tax secrecy laws. But because Wiese’s matter surfaced in an open court, the public is afforded a rare view of the role that supposedly reputable lawyers and tax advisers play in helping large companies and the wealthy avoid paying tax.

This is a privilege not enjoyed by ordinary citizens and smaller companies that cannot afford the services of firms like ENS.

Tullow goes Dutch

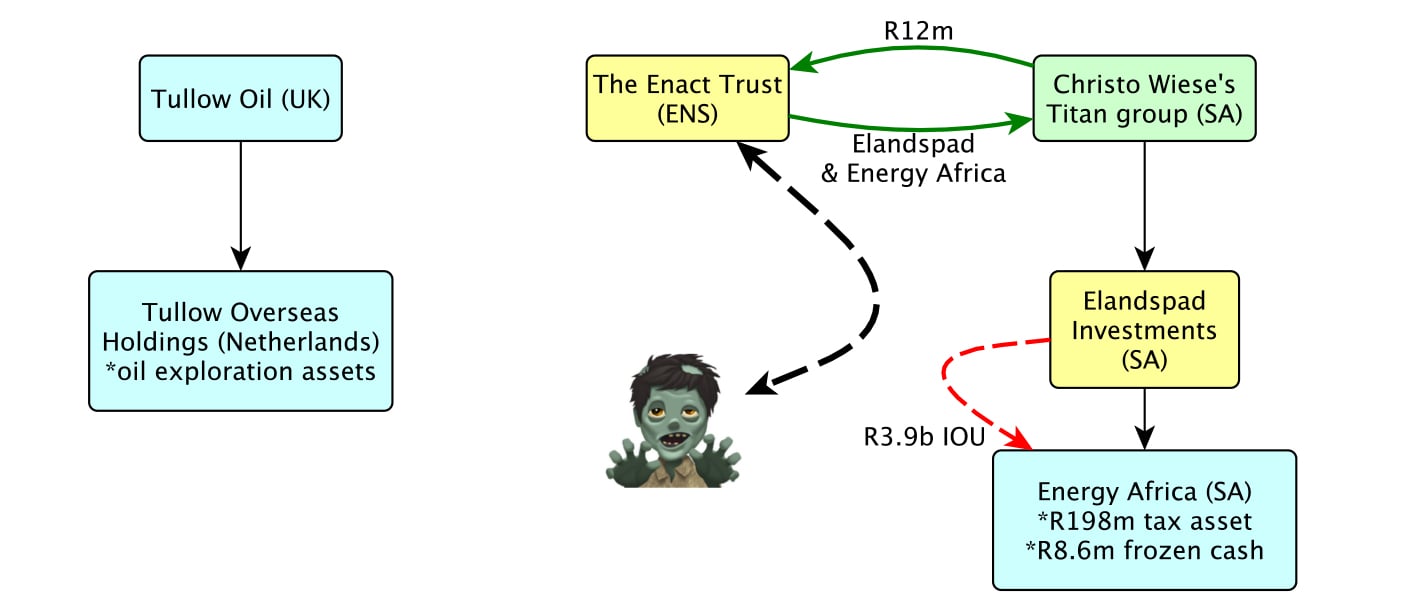

The fight goes back to January 2007. At the time, Tullow wanted to move a number of its international oil exploration assets into the hands of its Dutch subsidiary to “streamline the holding structure and erase inefficiencies and impracticalities”. Most likely, it also wanted to get the tax benefits from the Netherlands.

However, among Tullow’s assets were a number of African exploration ventures, which it owned through an SA company called Energy Africa Lt d .

The cheapest and most transparent way to get those assets to the Netherlands, Sars later argued, would have been for Tullow’s Dutch arm to simply buy them directly from Energy Africa.

Instead, ENS proposed a more convoluted solution, which Sars later argued was a “sham” that made no commercial sense. Sars said this structure was nothing more than “an elaborate scheme intentionally designed to facilitate the evasion of [capital gains tax] and [secondary tax on companies, a tax on dividends]”.

ENS rejected this. It argued that Tullow’s commercial rationale was legitimate and that it was allowed to arrange its affairs in the most tax-efficient manner.

The players

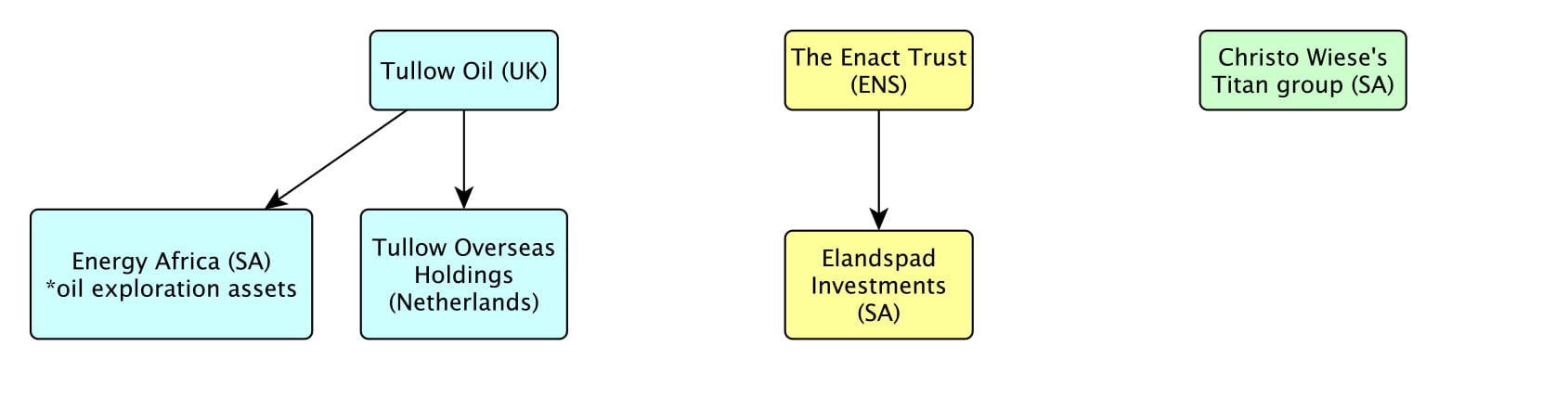

While a number of companies were involved, the three pivotal controlling hands were Tullow, ENS and, later, Wiese’s investment group, Titan.

Unusually, ENS itself had skin in the game through a vehicle called the Enact Trust. According to Sars court documents, Enact ’s trustees and beneficiaries were certain ENS partners, directors and employees.

Quite who they were ENS isn’t saying. Dachs refused to identify them, nor would he explain the exact nature of the trust and its relationship with ENS.

And, even though trust deeds are public documents, the master of the high court in Cape Town refused to allow us to inspect the Enact Trust deed. This disturbing lack of transparency hasn’t helped ENS’s argument.

The restructure

The transaction is complicated, but it can be boiled down to three main steps. This is outlined in a web of “interdependent ” contracts between companies controlled by Tullow and ENS’s trust, all signed in one week in January 2007.

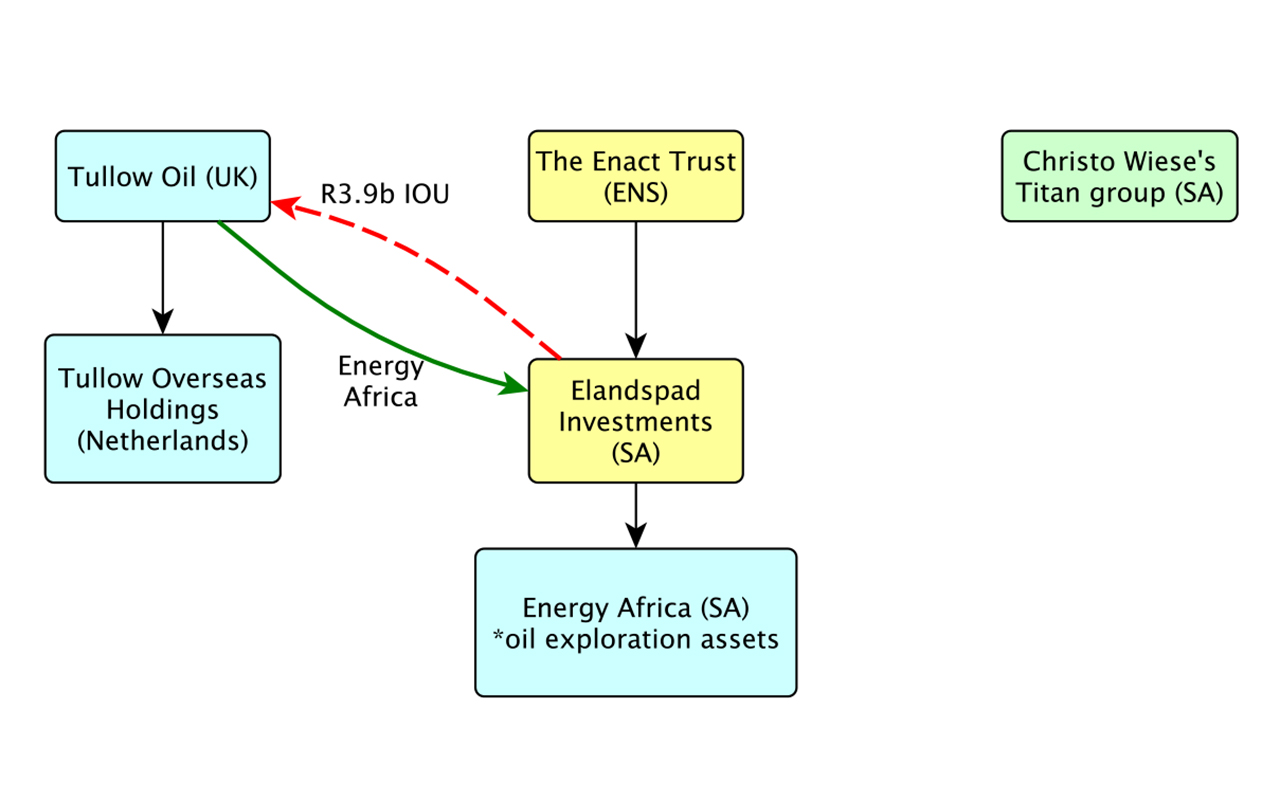

In step one, Tullow sold Energy Africa to the ENS-controlled SA company Elandspad Investments for $543.76m (about R3.9bn then). However, no money changed hands.

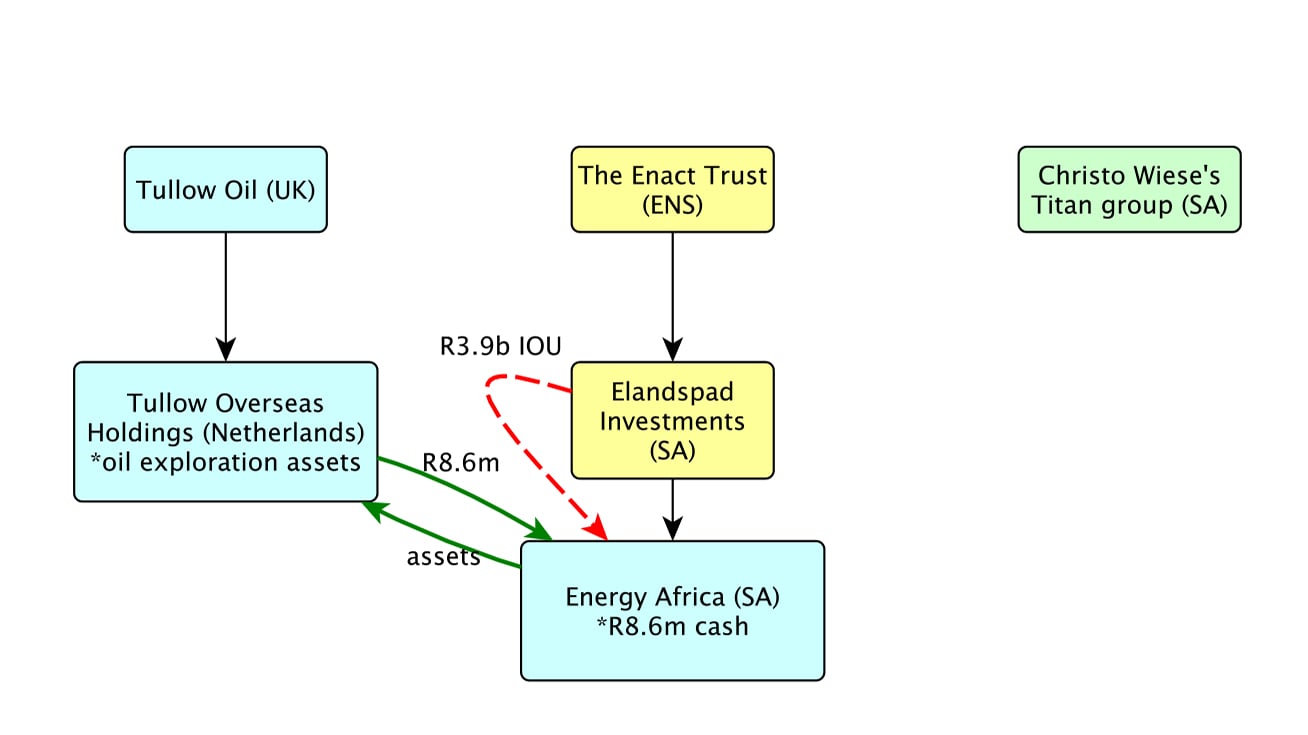

Instead the two groups set up a loan account a R3.9bn IOU from Elandspad to Tullow.

Step two: Tullow transferred that loan account to its Dutch subsidiary, which immediately transferred it to Energy Africa (by then in Elandspad’s hands) along with an extra $1.2m cash (about R8.6m then). In return, Energy Africa handed the oil exploration assets back to Tullow, now using its Dutch subsidiary.

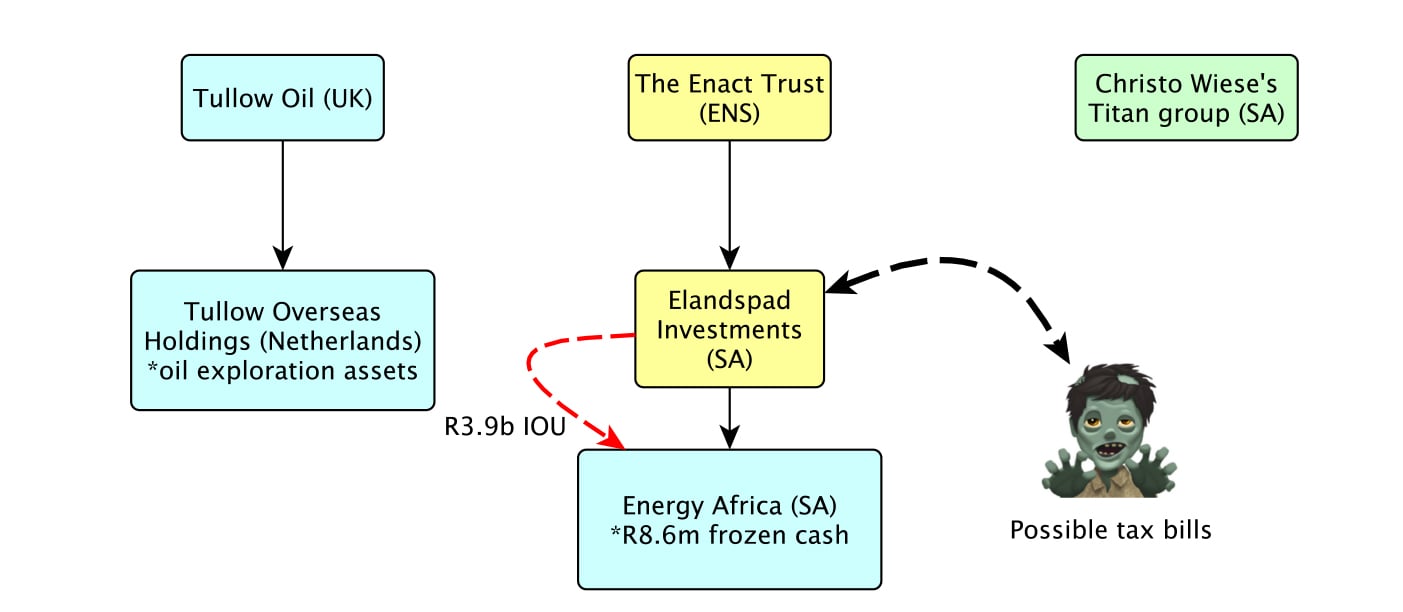

Actually, the R8.6m cash was frozen — Energy Africa could not touch it for three years, the contracts stipulated. Consider this transaction from Elandspad’s vantage point. It was now the owner of Energy Africa, to which it owed R3.9bn, but the assets that underpinned that obligation had been given to Tullow in the Netherlands.

All that was left was a cash shell, the Energy Africa holding company, and an account with frozen cash. It was a suspiciously bum deal.

As Sars put it: “It lacks commercial sense for parties to enter into a share sale agreement where the price is the same as the market value of an asset of the target company [Energy Africa] and the purchaser [Elandspad] will never enjoy any of the predominant commercial benefits of such asset. Yet this is precisely what happened” Sars concluded that: “Elandspad never intended to incur a bona fide liability in the amount of [R3.9bn] to a third party.”

Despite this, ENS was so confident of its structure that its company, Elandspad, even offered to indemnify Tullow against any future tax claims or liabilities in connection with the restructure. ENS, effectively, carried the risk.

‘Tax evasion’

So why the convoluted structure? In a series of letters, Sars claimed the agreements were simply part of an “elaborate daisy chain” designed to achieve some ulterior purpose.

“The unstated purpose of Tullow UK was to remove the underlying assets of the taxpayer from SA without paying [capital gains tax] or [secondary tax on companies],” it says.

ENS wrote back to Sars, denying this.

Rather, it said: “The [Tullow] restructure was the only reason the transactions were concluded at all.”

Sars believed the entire scheme was devised to “misuse or abuse” a local tax break called a “participation exclusion”. This allows a South African to sell shares in a foreign asset to a foreign buyer and bring that money home without paying capital gains tax.

However, this tax break is not allowed if the buyer and seller are connected parties and if the buyer does not pay the full price, among other conditions.

So, practically, if a Tullow company in SA sold a R3.9bn asset to a Tullow company in the Netherlands for only R8.6m, Tullow would have to pay capital gains tax.

But with ENS’s trust playing the middleman, Energy Africa and Tullow’s Dutch company were unrelated (on paper, at any rate) when the oil exploration assets were transferred from SA to the Netherlands.

And because Tullow’s Netherlands company had transferred a R3.9bn IOU to Energy Africa in return for the assets, a fee was paid — in theory.

Sars argued this was all “an illusion”. “The true substance of the transaction”, it said, was that Energy Africa and Tullow’s Dutch subsidiary were connected parties, while the R3.9bn price tag was also a simulation.

“The consideration, if the suite of agreements is looked at holistically, is the [R8.6m] paid by [Tullow’s Netherlands company] when the Tullow group ‘bought back’ it s own assets. That was the true consideration.

There was never any intention that the [shares in the assets] would be disposed of by [Energy Africa] for an amount equal to the [R3.9bn] valuation.”

In other words, the Sars official concluded, “I am of the view the ostensible consideration [R3.9bn] was a sham.” As a result, capital gains tax had to be paid, according to Sars.

And because assets worth about R3.9bn had changed hands between connected parties for just R8.6m cash, Sars considered the difference to be a dividend that Energy Africa had distributed to its “parent” Tullow.

Sars argued that the company paying this “dividend ” should also be taxed under an old provision known as a secondary tax on companies.

In its letters to Energy Africa, Sars said:

“With respect to the application of the doctrine of substance over form, it is the view of the commissioner that the taxpayer deliberately concealed the true substance of the transactions undertaken, and in doing so knowingly created a sham … with the intention of evading tax.”

Sars later calculated that the two taxes came to R940m. This, in addition to penalties of 150% plus interest, puts Sars’ claim now at R3.7bn.

Wiese’s little tax haven

It gets worse, however. The law firm’s new trust was now the proud owner of Energy Africa, but while their acquisition had given away its assets, it did still contain a trump card: an asset known as an “assessed loss”.

This is because, in previous years, Energy Africa had lost R198m, so it could theoretically write off future profits against this without paying tax. It meant the mysterious people behind the ENS trust could profit from this situation — which they did in step three.

In April 2007, three months after the Tullow restructure, an ENS man named Gert Viljoen approached Wiese with a proposition. Viljoen, then ENS’s “executive head: special projects”, had played a part in advising Tullow on its Dutch restructure.

A more recent ENS letter in the court file said Viljoen had “a longstanding relationship with [Wiese’s Titan group], spanning more than 15 years”.

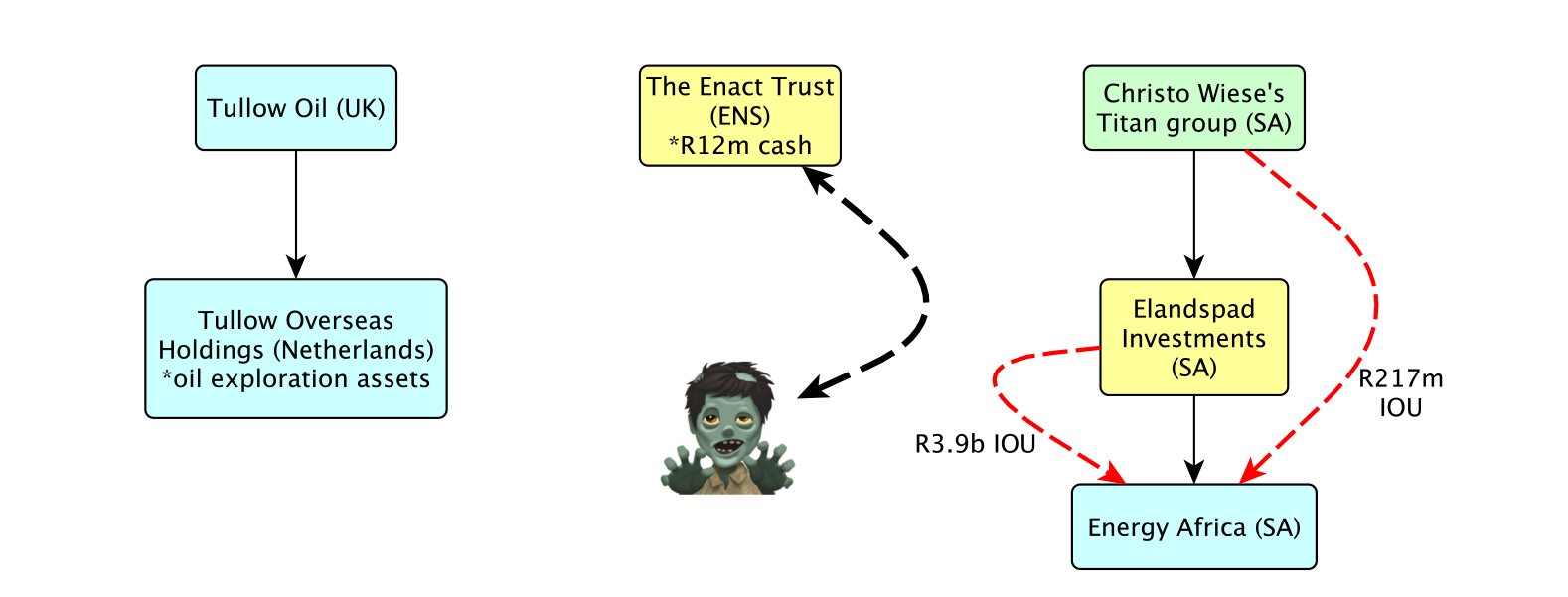

So on that day in April 2007, Viljoen acted “as representative of the Enact Trust” when he suggested that Wiese’s company, Titan Premier Investments, should buy Elandspad. Titan duly did so, paying R12m to Enact.

For Viljoen and ENS, this was an opportunity to release the value (and then some) tied up in Energy Africa’s frozen R8.6m. That money passed on to Wiese for use later, while he also became the proud owner of Energy Africa’s assessed loss, which he could then use for future tax write-offs.

Sars, however, says this was just another link in the “daisy chain” in which, it said, Tullow and Titan “bartered” tax benefits.

On Sars’ “bartering ” interpretation, Titan had helped Tullow to dodge taxes when it moved assets offshore, and in return, Titan got Energy Africa’s tax loss plus R8.6m cash.

In the process, Sars said: “The Titan group indemnified the Tullow group against any potential SA tax liability.”

But here, it seems Sars made an error. It had ignored the ENS trust’s role as a middleman, and it was Elandspad (effectively the ENS trust) that indemnified Tullow, not Titan.

ENS and Wiese jumped on this point, arguing strenuously against Sars’ interpretation. In an e-mail to amaBhungane, Wiese made two points: “First, the Titan Group had no involvement in the restructure by the Tullow group of its operations and there was no ‘trading of tax benefits’ between the Tullow and Titan groups.”

Sars disagrees.

In an earlier letter to Energy Africa, Sars said: “At the time of the assessment, the involvement of the Enact Trust was not known to the commissioner of [Sars]. [He] does not know the terms of the agreement whereby the transfer from the Enact Trust to Titan was effected … In any event, the assessment raised by the commissioner is neither founded on nor rendered invalid by the involvement of the Enact Trust.”

In any event, if Sars was to decide that Tullow dodged tax, Wiese wanted nothing to do with it. According to letters from ENS in the court file, Titan had bought Elandspad on condition that the ENS trust indemnified Titan from “any historic obligations or liabilities that may arise” from the Tullow restructure.

So the people behind the ENS trust appeared to remain exposed to any potential tax bills. In point number two of Wiese’s e-mail to us, he said: “Secondly, the Titan Group derived no tax benefit in respect of its subsequent acquisition of Energy Africa from Elandspad.”

Sort of.

In the court papers, Sars says that immediately after buying Energy Africa, Titan shifted R657m cash into Energy Africa, with which it traded in single stock futures. It also got an “inter group management fee” and other fees.

And every year that Energy Africa turned a profit, it wrote this off against Tullow’s old assessed loss and did not pay tax.

In a letter, Sars said: “The taxable income [Energy Africa] earned in the 2007 to 2012 years [after Titan bought it] amounts to approximately R200m, which dovetails with the assessed loss of approximately R198m. “The main objective of the Titan group [in buying Elandspad and Energy Africa] was to access the assessed loss. Once it had done so and exhausted the tax benefit of the assessed loss, it withdrew the activities it had introduced.

“The taxpayer is now dormant.”

Much later, Sars slapped Energy Africa with a R100m tax bill (including penalties and interest) “on the basis that the sole or main purpose for the Titan Group acquiring the shares in [Energy Africa] was to utilise the assessed loss”.

Titan ultimately paid Sars an undisclosed settlement for this. So, yes, Wiese might say that Titan “derived no tax benefit”.

Gunning for Wiese

To step back into our chronology, a few years after Tullow’s restructure in 2007, Sars went for Wiese’s throat. It appears this was sparked by an unfortunate incident Wiese had in London.

On April 27 2009, Wiese tried to board a flight from London City Airport to Luxembourg, carrying £120,000 cash in his carryon luggage. He had also stuffed another half a million pounds (about R9m then) into his suitcases.

Customs officials stopped him and took the money.

Wiese reportedly told them these were profits from his diamond deals back in the 1980s, and that he was off to invest the money in Luxembourg.

Wiese fought in a British court and eventually got the money back. But according to later news reports, the scuffle sparked interest from Sars, leading to a big audit.

A year and a half after the London bust, the first tax bill landed at Energy Africa’s door. This was for its use of the assessed loss, discussed previously.

Nearly a year later, in August 2012, City Press and the Sunday Times announced in tandem that Sars had slapped Wiese with a R2bn tax bill. It is unclear if this was related to the Energy Africa affair.

The next month, Sars sent Energy Africa another R20m bill, and in November the big one landed: a 32-page letter from Sars’ Large Business Centre in which officials explained their audit of the Tullow restructure, and they notified Energy Africa that they intended to claim R940m in unpaid tax, plus penalties and taxes (now R3.7bn).

The Large Business Centre at Sars was a highly specialised unit that dealt with SA’s biggest, most complicated taxpayers: large corporates like Tullow and “high net worth individuals” like Wiese. It collected about a third of Sars’ revenue.

Recently, the former head of the centre, Sunita Manik, publicly accused former commissioner Tom Moyane of undermining and dismantling it. Moyane has denied this.

In an e-mail to amaBhungane, ENS’s Dachs tried to explain that Sars did not base its technical case on a charge of “tax evasion”.

Tax evasion is a criminal offence as opposed to “av o id a nce”, which is sometimes allowed and sometimes not. However, it is easier for a revenue collector to sustain an allegation of avoidance.

One person sympathetic to ENS who knows this case well told us that Sars will often accuse a taxpayer of evasion when it is arguing for a big penalty, even if the underlying claim is of avoidance. He said this was what Sars did in Energy Africa’s case.

Said Dachs: “In respect of the merits,” — he underlined this part in the e-mail to us — “Sars has never alleged or argued that the restructure transactions constituted a ‘tax evasion scheme’.”

Instead, he said Sars argued that the “substance over form” doctrine applied to thetransactions and, alternatively, that the general antitax-avoidance rules applied to the transactions.

Wiese tries to wash his hands

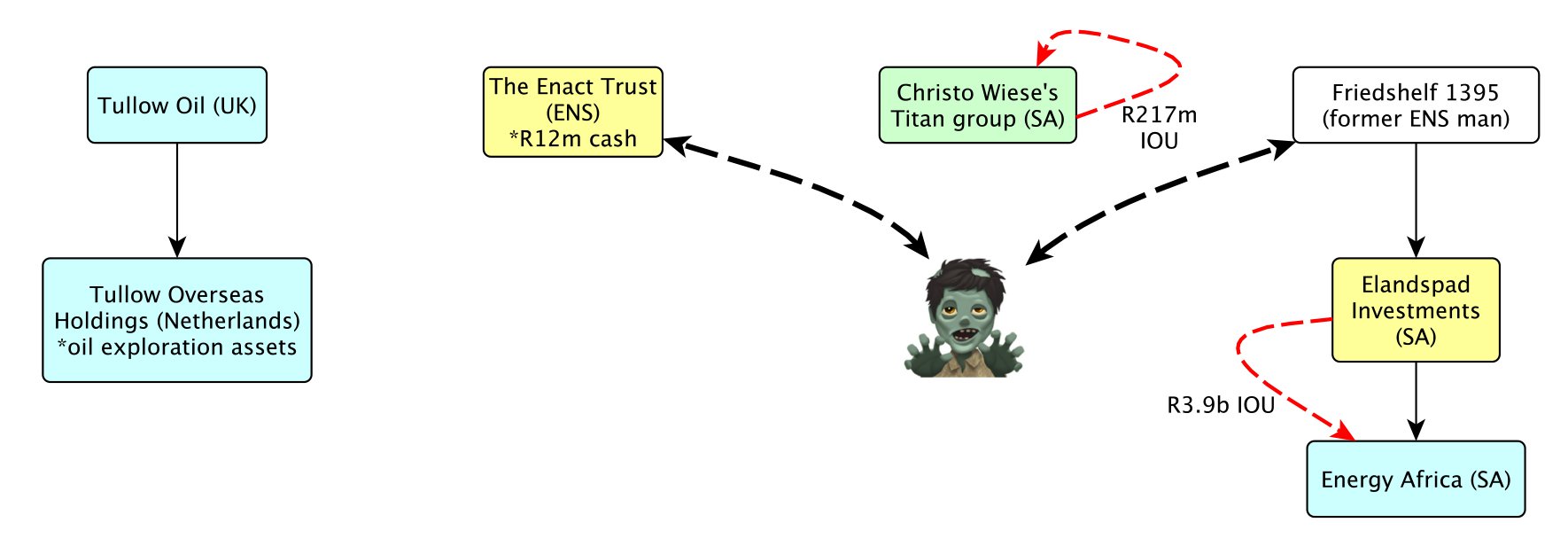

Meanwhile, Gert Viljoen left ENS in 2011 to start his own boutique financial advisory firm, nestled on the first floor above a famously trendy bakery and coffee shop in Bree Street, Cape Town.

It was Viljoen who sold Wiese the scheme in 2007 on the condition that, should Sars come knocking concerning Tullow’s tax affairs, it would not be Titan’s problem.

Then Sars had come knocking — and Wiese sent someone from Titan to tell

Viljoen. Wiese’s man “requested” that Viljoen take over Elandspad and Energy Africa “to deal with such an inquiry”, according to letters in the court file.

Viljoen was ready to oblige.

Writing to Sars on his behalf much later, ENS said: “It was relevant for Mr Viljoen” that Titan had major interests in Shoprite, Steinhoff International Holdings and Pepkor Group.

“Mr Viljoen thus considered it in the interest of his business to acquire the shares in [Energy Africa] as requested by [Titan].”

In other words, Viljoen’s fledgling outfit relied on Wiese’s business.

As ENS put it: “Mr Viljoen considered himself, together with ENSafrica, to be best placed to deal with Sars’ inquiries.” So Viljoen and ENS prepared themselves for a R3.7bn fight.

In April 2013, five months after the Sars Large Business Centre’s letter, ENS’s Dachs replied, setting out why his client, Energy Africa, believed the tax claim was baseless.

Three days later, Wiese resigned from the Elandspad and Energy Africa boards. There was another twist: at the time, one of Titan’s group companies still owed Energy Africa R217m for some unfinished business, even though Wiese ultimately owned both.

But before handing the Energy Africa lemon back to Viljoen, Wiese wanted to ensure he kept this R217m loan asset.

As ENS explained to Sars: “As Dr Wiese did not wish for a third party to hold a claim against [Titan], it was decided that [Energy Africa] would distribute the loan claim to Elandspad, and thereafter, Elandspad would distribute [it to Titan Premier Investments], whereafter the shares were sold.”

So in a nutshell, Energy Africa declared the money as a dividend to its erstwhile parent, Titan. This ensured the R217m loan asset remained with Wiese’s group, rather than going with Energy Africa to Viljoen. After that was done, Wiese signed the papers to transfer Elandspad, Energy Africa (and hopefully the tax woes) to Viljoen.

Still, Sars was unmoved by Dachs’s arguments and issued a “finalisation of audit” letter in August 2013.

Dachs ’s colleague wrote back to say Energy Africa still disputed the claim. Anyway, it “does not have cash or assets and … is therefore not able to make payment of the disputed tax”.

In June 2014, Sars issued a “final demand” that Energy Africa should pay its tax debt within 10 days. But Viljoen wrote back to say Energy Africa was dormant.

The shutters were drawn. The money was gone.

The illusion

To put this in context, it was in November 2012 that Sars first told Energy Africa it believed the R3.9bn price tag for the Tullow assets that went to the Netherlands was a “sham”, a “simulation” and an “illusion”.

While ENS disputed this, Energy Africa’s 2013 and 2014 audited financial statements underscore the apparent absurdity of ENS’s structure.

The financials, both published in April 2015, show that, up to 2013, Elandspad owed Energy Africa R3.9bn; but the next year, Energy Africa simply wrote it down to R1.

This meant that for seven years from 2007, a R3.9bn “debt ” based on assets that had long since gone to Tullow’s Dutch company remained on Elandspad and Energy Africa’s books, before vanishing in a puff of accounting smoke.

Personal liability

In February 2016, Sars liquidated Energy Africa through the Western Cape High Court.

In October that year, Sars sent notices to Wiese, Viljoen and two of their colleagues, seeking to hold them personally liable for the R217m asset they had allegedly “knowingly dissipated … in order to obstruct the collection of the [R3.7bn] tax debt”.

ENS ’s Dachs fought this, on behalf of all the parties. Dachs wrote that when Energy Africa’s assets were spirited up to Titan, Wiese “entertained the good faith belief” that Sars was wrong and no tax was owed.

“Dr Wiese placed reliance on the representations and warranties obtained from the Enact Trust at the time,” the lawyer said.

This included the warranty that when Tullow restructured, “advice was sought from tax advisers, and opinions were obtained from senior counsel who confirmed that no [capital gains tax] and [secondary tax on companies] implications should arise”.

In any case, ENS argued, Wiese had resigned from Energy Africa the day before the alleged “dissipation”. Sars rejected this, calling it a “contrived argument”.

“To put it plainly, you sought to drive a wedge between the Titan group and that of the problematic taxpayer [Energy Africa] and to prevent Sars from laying its hands on the only remaining asset of the taxpayer,” it said.

In fact, Sars argued, the “clear purpose” of Wiese, Viljoen and the others was to “delink the taxpayer (and hence its tax liability) from [Titan].”

In August 2017, Sars wrote to Wiese, Viljoen and the two others, demanding payment of the R217m within 10 days. Three weeks later, a high court sheriff served them with summonses.

Wiese and the others filed an “exception” which is a technical objection — with the court. They claimed Sars had failed “to allege any facts in support of the allegation made” that they’d had knowledge of obstructing the collection of tax.

Sars’ claim was so vague, they argued, that they could not defend themselves against it without being prejudiced. This argument will be heard in the high court in Cape Town on August 22.

ENS

When amaBhungane asked Sars if it was pursuing ENS or those who controlled the Enact Trust or the Tullow Group for their role in this alleged tax-evasion scheme, Sars said it did not comment on taxpayer information in the public domain.

“Sars is bound by the confidentiality clause, that is, section 69, not to divulge specific information and details on the affairs of taxpayers,” it said.

However, Dachs told us that Sars “has all the relevant facts in relation to the role of each of the advisers in relation to these transactions. Sars has not sought to impugn the role of any of the advisers arising from these transactions.”

And we asked Wiese: “It strikes us that ENS/the Enact Trust sold you a very sour lemon (R3.5bn sour). Do you wish to comment on: (a) if you have received advice on whether you have a claim against the firm or its agents? and (b) whether ENS is representing you for its own account (gratis to you)?”

He responded: “Dear Sam. The answer to both of your questions is no. Regards, Christo Wiese.”

The amaBhungane Centre for Investigative Journalism produced this story. Like it? Be an amaB supporter and help us do more. Know more? Send us a tip-off.