In the first of this two-part series, we explored how offshore diversification works to reduce the inherent risk of one’s portfolio and to help shield against losses. These risk-busting benefits tend to hold true regardless of what is going on in the world, or where you call home.

Yet there remains an important element to the space dynamic of risk: time.

Speak to any investment professional today, and they will tell you that the market turbulence of 2020 reminded us of a key principle — the importance of staying true to the course of one’s long-term investment plans.

In the wake of a sharp economic recession, sparked by the rapid spread of Covid-19, equity markets across the globe shed enormous value in the first parts of 2020. Yet, following the initial panic, most major developed and developing markets soon recovered.

As a general rule, investors who had held fast through the turbulence of the year would have fared far better than those who reacted emotionally and exited the markets during its initial dip.

The volatility caused by Covid-19 was extreme. However, in the short term, markets should always be expected to be unpredictable, and highly erratic. Add in the rapid up-and-down movements of the rand exchange price, and the performance of one’s offshore investments can, at times, seem dizzying.

When viewed from a longer-term perspective, however, these unpredictable movements tend to be replaced by reliable trends. Therefore, it is important to keep one’s focus on the not-so-distant future, rather than the immediate past.

The importance of time in the market

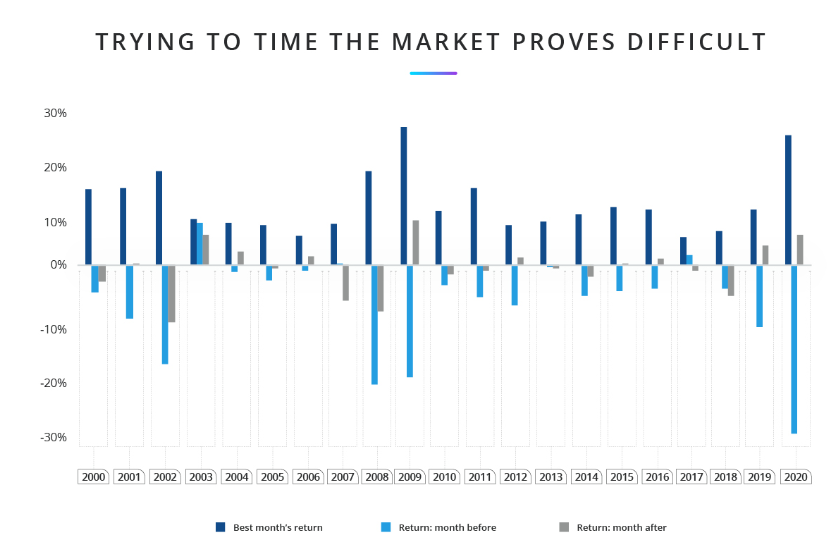

We conducted an analysis from 2000 to mid-2020, ahead of the strong year-end-recovery experienced by markets globally. The aim was to illustrate the danger of attempting to time the market, no matter what cycle it appears to be in.

The chart below describes the best returns for each month of the year of the United States Standard and Poor’s 500 (US S&P 500) Index, and plots these in the blue bars. The S&P 500 tracks the combined performance of 500 of the largest companies listed on US stock exchanges, making it one of the most monitored indexes in the world. The orange bars describe the returns achieved in the month before these best months, and the grey describe the months just after.

A quick glance and it becomes clear just how erratic markets tend to be. With months of top performance typically characterised as a rebound from preceding months of poor performance. Reacting emotionally and exiting markets when the going gets tough can often prove to be a devastating mistake.

Another way to visualise this is to calculate for the compound effect of missing out on only the best five days of market performance each year.

To do this, we constructed two hypothetical portfolios and plotted these in the chart below.

In this simple example, the blue line describes the returns for an investor who remained invested in the S&P 500 for a decade, from 2010 to 2020. The orange line describes the returns for an investor who had missed out on just the five days of best performance each year.

The hypothetical investor who remained invested for the full 10-year period until 2020/07, earned a total growth in the value of their investments of 249.5%. The investor who missed just the best five days in each year, saw their investment value decline by 22.5% in nominal terms.

The message is clear: staying the course over the long term in an adequately diversified portfolio, while allowing compounding to take effect, is the critical combination to reach one’s investment goals.

When emotions meet markets

Remaining invested for the long term is a crucial principle that applies to the vast majority of investors. However, there are several biases that are shown to lead even the most seasoned investment professionals astray.

Loss aversion, for example, tends to distort our perception of risk-and-reward relationships. The consequence of this is that many investors tend to weight their portfolios too heavily in less volatile, more conservative assets, such as cash. Due to this, they forego the expected long-term outperformance in the equity markets.

This is, in part, due to what we term a fallacy of risk. This refers to the reality that, paradoxically, investing too heavily in assets seen to be low risk creates a higher risk that investors will not achieve their long-term goals.

Hindsight bias, meanwhile, is the tendency of investors to overweight the recent performance of markets and funds when making estimations about future performance. As we have seen, this can have severe consequences when the markets go through their inevitable dips.

There are many other such biases that combine to create the reality that many investors subconsciously choose to grow their returns by less and to exacerbate their losses.

Our unique shared-value approach to investing is designed to combat many of the well-documented cognitive biases that are proven to undermine the long-term performance of one’s portfolio. We do this through a system of rewards that work to counteract emotionally driven investment behaviours and are designed to help our clients stay on course to achieve their long-term investment goals.

Craig Sher is Head of R&D at Discovery Invest