Protests: Turkey has seen opposition to the country’s declaration of ‘an economic war of independence’ by refusing to rein in inflation using higher interest rates and other measures. (Yasin Akgul/AFP/Getty)

A currency meltdown, rocketing inflation, civil unrest. This is the current picture of Turkey’s economy, whose president Recep Tayyip Erdoğan has declared “an economic war of independence”.

Erdoğan’s gamble, which uses monetary policy to drive investment and job creation, is not one that many are willing to take. Faced with fears inflation will become entrenched, pushing advanced economies to withdraw accommodative monetary policy, most emerging market economies have gone in the opposite direction. While the Turkish central bank aggressively slashes interest rates, others, including South Africa, have started to raise theirs.

For emerging market countries like Turkey and South Africa, economic independence is hard won, analysts say — especially considering how vulnerable they are to financial market volatility.

Critics of Erdoğan have pointed out that inflation, if not kept in check by higher interest rates, will drive up the cost of Turkey’s heavy imports. The country, which under Erdoğan has pursued a programme of building mega projects using foreign money, also has a corporate debt problem. A weak currency stands to make the country’s foreign debt far more onerous.

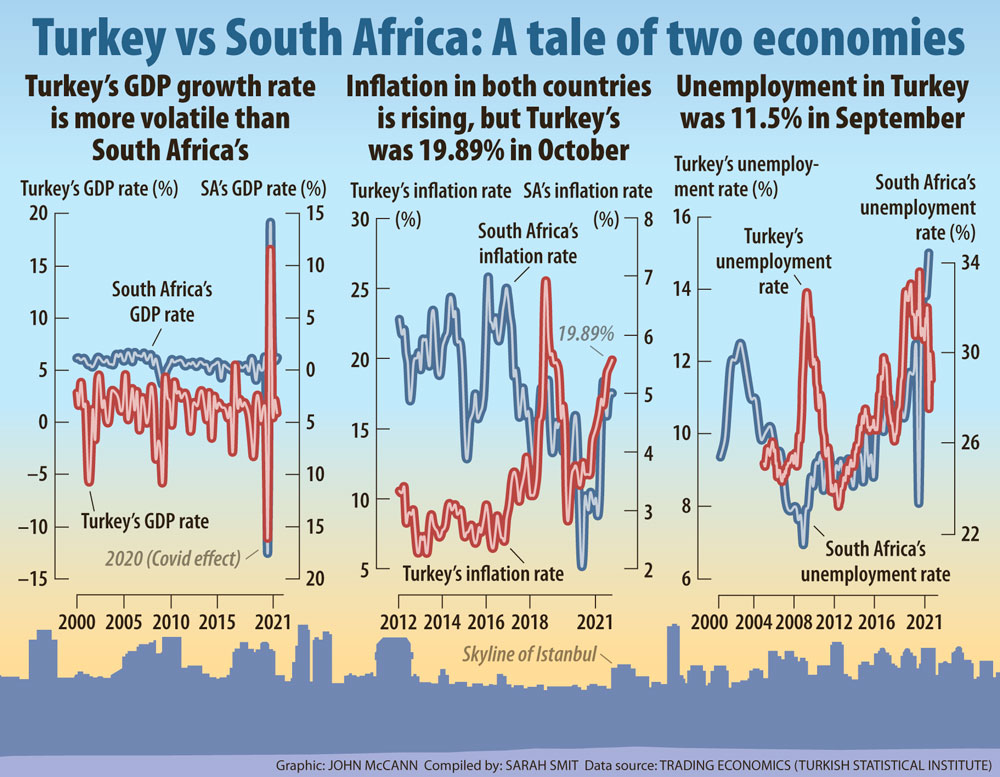

But Erdoğan has been steadfast about using record low interest rates to grow the economy in the face of financial market pressures that threaten to crash the Turkish lira, which has depreciated 38% in the year to date against the US dollar.

Turkey’s unorthodox stance on monetary policy, which has reportedly been driven by a trigger-happy Erdoğan, comes as emerging markets weigh the prospect of high inflation against the desire to dig their economies out of a growth freefall induced by the Covid-19 global pandemic.

In 2013, South Africa and Turkey were both listed among what then Morgan Stanley chief executive James Lord dubbed “the fragile five”. The moniker was used to describe countries that rely heavily on foreign speculative investments, thus making them vulnerable to changes in the global financial landscape: “High inflation, weakening growth, large external deficits and in some cases exposure to the China slowdown and high dependence on fixed income inflows leave these currencies vulnerable, in our view.”

In 2013, Turkey’s economy grew at an annual rate of 8.5% and hasn’t expanded at that pace since. Erdoğan became president in 2014. The country’s GDP has declined over the last eight years. However, the Turkish economy grew by 21.7% in the second quarter of 2021 — the highest growth figure since 1999.

Turkey’s unemployment rate has generally trended upwards since 2013, when the country recorded a jobless rate of 8.73%. In 2020, Turkey recorded an unemployment rate of 13.92%, the highest since 1999.

But, unlike in South Africa, Turkey’s joblessness has since fallen. This week, data revealed that South Africa’s unemployment rate has reached a staggering 34.9%.

Earlier this month the South African Reserve Bank’s monetary policy committee decided to follow the lead of its emerging market peers, like Brazil and Chile, and lift interest rates. The Reserve Bank immediately faced criticism for putting the brakes on the country’s already stalled economic growth by dialling back accommodative monetary policy.

But Isaah Mhlanga, chief economist at Alexander Forbes, pointed out that South Africa’s monetary policymakers are not tasked with “economic growth as its headline objective”.

“Economic experimentation will only be necessary once you have implemented the existing policies and they haven’t delivered what they are supposed to deliver,” Mhlanga said, adding that Turkey was “shooting itself in the foot”.

“What they are doing is not economics. It’s pure politics,” he said.

Maxim Rybnikov, a director in the Europe, Middle East and Africa sovereign ratings team at S&P Global, noted that Turkey’s economic policy has tended to be “erratic and unpredictable”, resulting in elevated financial market volatility.

Noting what happened during Turkey’s 2018 currency crisis, which triggered a slowdown in economic activity, Rybnikov said: “The way economic policy is done in Turkey is not particularly conducive to resolving economic imbalances to getting inflation down and to get the country on a sustainable growth path.”

The strengths of the Turkish economy — such as a low net general government debt and a relatively vibrant private sector — may see it faring the current volatility as it has done in the past, Rybnikov said. “But it will not be because of the government’s economic policies, but despite the policies.”

(John McCann/M&G)

(John McCann/M&G)

Dick Forslund, the senior economist at the Alternative Information and Development Centre, said Turkey’s current currency woes may have been averted if the country had tighter capital controls — which regulate flows from capital markets into and out of a country’s capital account, thus insulating the currency from financial volatility.

Forslund cited John Keynes, the originator of Keynesian economics, who said: “In my view the whole management of the domestic economy depends on being free to have the appropriate rate of interest without reference to the rates prevailing elsewhere in the world. Capital controls is a corollary to this.”

Turkish Marxist economist E. Ahmet Tonak said that ideally Turkey would have implemented a policy of capital control prior to the recent devaluation of the lira. “However, the current regime cannot and does not implement such a policy for obvious reasons,” he said.

“They think that they will be able to attract foreign hot money to solve the rapid deterioration of the lira. No foreign speculator would go to a country where there is capital control. Moreover, most of the significant domestic foreign currency holders probably already parked their money abroad. Hence, from the current government’s point of view, capital control policy is not implementable under the current circumstances.”

Rybnikov said capital controls will likely be “a measure of last resort” for Turkey. “Experience from other countries suggests that after you put capital controls in place, you might want to remove them very quickly. But usually it takes many years,” he explained.

“And of course, it is a distortionary economic policy, which usually can lead to lower desire among investors to invest in Turkey, for obvious reasons: You’re not going to invest if you are not sure how you are going to get out. It’s not going to be particularly politically popular among domestic residents.”

Political economist Patrick Bond explained that South Africa doesn’t have tighter capital controls because of the ideological pivot towards liberalisation post-1994. “It was part of the whole transition in which a power network pushed South Africa into the world economy much faster than was advisable.”

The post-apartheid dispensation, Bond said, “made way too many concessions to international capital and financial capital was becoming dominant. This was the beginning of the era of neoliberalism. The ideology was, if you let money flow faster in and out of your country, then you’ve got more confidence from international investors.”

Tighter capital controls will likely only be implemented under a post-neoliberal government, Bond said. In order to bring about some sort of economic independence from global financial pressures, he surmised, emerging market economies need “a new generation of leadership”.

[/membership]