Eight insurance firms are being probed over price-fixing allegations. Legally, clients can claim for damages but experts say they should not hold their breath

The eight insurance companies that are being investigated for collusive practices could, in theory, face a class-action suit by affected clients, if found guilty. However, precedence suggests such a path would not be smooth sailing for the complainants.

Competition authorities are probing Old Mutual, Sanlam, Discovery, BrightRock, FMI, Hollard, Momentum and the Professional Provident Society for alleged collusive behaviour and recently conducted searches at their premises.

The Competition Commission said it had “reasonable grounds to suspect” the insurers had worked together to fix prices and/or trading conditions regarding fees for investment products such as retirement annuities and premiums for risk-related products.

If the insurers are found to have contravened the Competition Act and engaged in collusive practices, consumers can claim civil damages, according to Werksmans director Ahmore Burger-Smidt, who cautioned, however, that this would not be easy.

A class-action lawsuit is one where one person or a group of people pursues an action on behalf of a group. If this is successful, all the members of the class benefit.

“The problem in instituting a class action as a consumer is that you have to demonstrate the damages suffered … The big hurdle in all of this is how to quantify the damage for everyone involved,” Burger-Smidt said.

Because everyone in the class is affected differently, she explained, it is difficult to present a case that satisfies everyone and ensures they receive adequate damage claims.

“In all the years that we’ve had a competition authority we haven’t seen a class action taking any solid form and moving forward, because a class action must be certified to move forward.”

According to Bowmans’s Class Action Litigation Guide, the first stage of class actions is a certification application. South African law requires that, before a class action can be instituted, the potential plaintiffs must obtain permission from a court, resulting in certification.

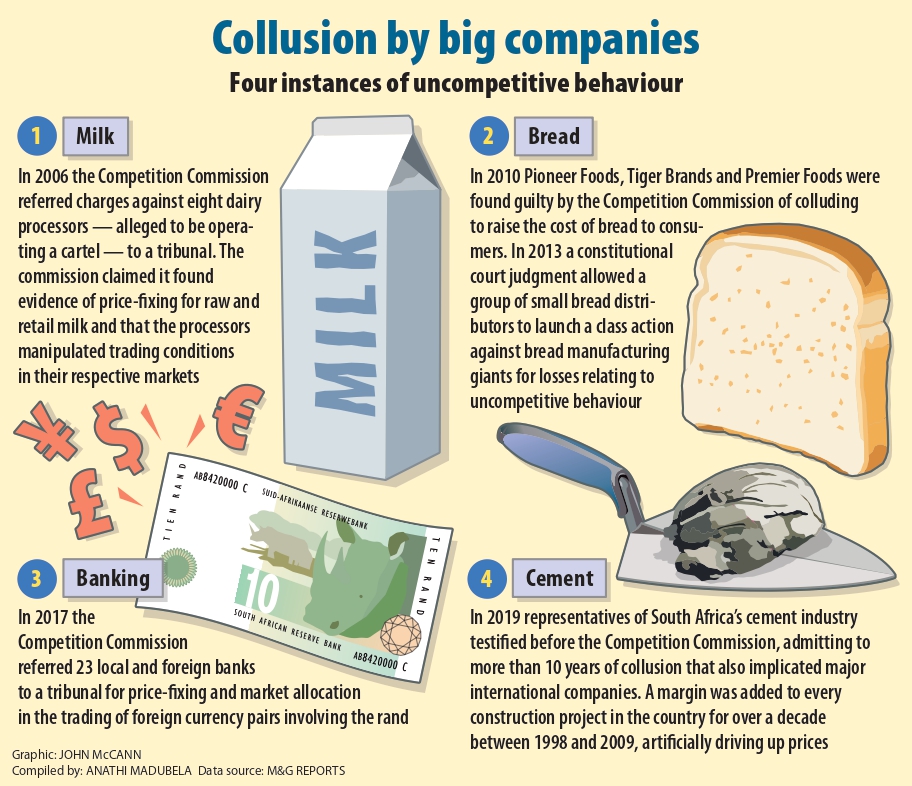

“Historically, there were attempts to form a class action with the bread cartel but that didn’t really go anywhere,” Burger-Smidt said.

In 2012, small bread distributor Imraahn Ismail Mukaddam and others applied to the high court to bring a class action for damages against Pioneer Foods, Tiger Brands and Premier Foods. The three manufacturers had been found guilty of anti-competitive behaviour, including fixing the price of bread, by the Competition Commission in 2010.

The supreme court of appeal (SCA) held that Mukaddam had failed to establish exceptional circumstances for instituting a class action.

The constitutional court said the SCA had applied the incorrect test when deciding on the prior certification of the class and overturned the rulings of both the high court and the SCA.

According to Professor Phumudzo Munyai, head of mercantile law at the University of Pretoria, collusion, particularly price fixing, is a form of theft or corruption and the initial step for recourse by affected parties is investigation and then a prosecution before the Competition Tribunal. If the guilty parties appeal an unfavourable decision by the Competition Tribunal, the next step is the Competition Appeal Court.

“Once the competition litigation process is completed successfully by the competition authorities, parties (including customers and consumers) affected by collusion may sue the offending firm(s) in the high court for damages. This is where class action can be considered as a vehicle to claim damages by, or on behalf of, customers or consumers affected by collusion,” he said.

But Munyai agreed with Burger-Smidt that the viability of class action in South African competition law has always been an issue of concern from a consumer perspective.

“There have been some class-action suits in South African competition law. But none of the competition law class-action suits brought before a South African court were ever successful,” he noted.

“The reasons for this include difficulty in identifying customers or consumers belonging to the class or group on whose name the action is to be taken; the appropriate class action design to litigate the case on behalf of affected customers or consumers; proving actual damages suffered by affected customers or consumers and establishing a causal link between the price charged and harm suffered by the end-user consumer.”

How it affects customers

“The one thing that always happens when there are collusive practices occurring, like price fixing or the fixing of trading conditions, is that, inevitably, either the consumer will pay a higher price for a product or the consumer will get a lower-quality product, or a combination of this,” Burger-Smidt said.

In the latest case, the Competition Commission says the insurers have been sharing information on premium rates for risk-related products and fees for investment products, including dread disease, disability and life cover; funeral assistance benefits and retirement annuities.

The commission says it has “reasonable grounds to suspect” that this information-sharing enabled the insurers to adjust the prices of their existing products and new policies.

“One of the worst crimes towards the consumer is cartel behaviour …this is a stock standard, fundamental competition law principle. And that is one of the core reasons why the competition authority ought to be there to protect consumers from higher prices and lower-quality products,” Burger-Smidt said.

The Competition Act prohibits an agreement between competitors that has the effect of substantially preventing or lessening competition and also outlaws the direct or indirect fixing of a purchase or selling price or any other trading conditions.

According to Munyai, collusion leaves the poor, in particular, worse off, as they might be faced with higher prices. It is a classic case of the richer getting richer and the poor getting poorer.

“When this scenario is also considered in the context of present-day realities in South Africa — of poverty, unemployment and rising cost of living — the pervasive impact of collusion cannot be overemphasised. It is for this reason that collusion is considered ‘the most egregious of all competition-law violations’,” he said.

(John McCann/M&G)

(John McCann/M&G)

What can the state do?

“Part of what the competition authorities are empowered to do is institute an administrative penalty which goes to the fiscus and that in itself is already deemed a significant deterrent for anti-competitive behaviour,” Burger-Smidt said, referring to a fine of about 10% of the offender’s turnover for a specific period.

“Historically, it is not 10%, it’s up to 10% and it’s sometimes around 8%. Various arguments will be submitted in terms of determining the specific fine that will be allocated, she said.

The state could do more in terms of legislation, Burger-Smidt believes.

“If we compare the Competition Act to the Protection of Personal Information Act, the latter allows for the information regulator to institute civil damages on behalf of affected subjects, whereas the Competition Act, being a much older piece of legislation, does not have that provision.”

Besides the massive administrative penalties, there are other measures available as part of the state’s arsenal against collusion, Munyai said.

“The Competition Act creates a cartel crime, in terms of which executives of firms found guilty of collusion may personally be charged for causing their firms to engage in collusion. In terms of the Act, company executives who are found guilty of having caused their firms to engage in collusion may face imprisonment for up to 10 years or a fine of R500 000 or both fine and imprisonment combined, as a package, in a single punishment,” he said.

But the provision has not yet been put into use in practice and, as such, no single company executive has ever been sent to jail for causing their firm to engage in collusion.

“Because this is a criminal provision in nature, it will naturally and constitutionally require the involvement of the National Prosecuting Authority in the prosecution process. There are doubts, however, whether the NPA has the technical skills to prosecute competition-law related offences,” Munyai added.

Not guilty … yet

The competition authority conducted the recent search-and-seizure operations as part of an investigation that started in January last year. During the searches, it seized documents and electronic data, which will be analysed together with other information gathered, to determine whether the insurers have colluded.

Burger-Smidt noted that the mere fact that the commission had conducted a raid did not mean the insurers were guilty.

“There is still a long way before we can get to a prima facie case. At the moment, they’ve got a reasonable suspicion and that is what we are looking at. If, one day in the future, parties are found guilty of collusive behaviour only then will it necessitate a change in behaviour,” she said.

As shown in the recent Competition Commission v Irvin and Johnson Limited and Karan Beef (Proprietary) Limited case, the commission has the burden of proof on a balance of probabilities. That means it must prove the conduct of the insurers contravened the Competition Act.

In the Irvin & Johnson case, the commission alleged I&J had entered a collusive agreement with Karan Beef. It lost this case after the Competition Tribunal dismissed it for lack of evidence.

“Only if they (the insurers) are found guilty will the companies be forced to reconsider the way they behave and the way they conduct themselves in line with the legislation. We are not looking at guilty parties — yet,” Burger-Smidt said.

Anathi Madubela is an Adamela Trust business reporter at the Mail & Guardian.

[/membership]