Unemployed men inJohannesburg wait on a street corner for work for part-time work. Photo: Naashon Zalk/Bloomberg/Getty Images

ANALYSIS

Next week Finance Minister Enoch Godongwana will deliver his budget speech, the last before an election that will have South Africa’s economic crisis at its heart.

The day before Godongwana’s speech, Statistics South Africa will publish the country’s unemployment numbers — the news of which will probably be eclipsed by the minister’s appraisal of our fiscal predicament.

These crises — the country’s squeezed public finances and its extreme unemployment rate — are linked, although the latter may only get a cursory mention in the budget.

On the Tuesday before the 2022 budget, the release of the quarterly labour force survey was abruptly postponed so that StatsSA could conduct certain quality checks.

That year, the treasury’s tone was decidedly more positive than it had been during previous budgets. Then director general Dondo Mogajane wrote in his foreword that there was “a light at the end of the tunnel”, signalling the imminent end to a difficult period of fiscal consolidation.

Despite this change of fortunes, that budget contained one startling confession. Referring to the economic onslaught from the Covid-19 pandemic, the document noted: “There is a real risk that many of the jobs eliminated will not return.”

The postponed labour force data was eventually published, showing that South Africa’s official unemployment rate had risen to 35.3% in the fourth quarter of 2021 — the highest on StatsSA’s record.

Although this number has come down, the jobless rate remains among the highest in the world at almost 32%. And, as the country’s fiscal policymakers continue to inflict austerity, the likelihood that the economy will create substantially more jobs is slim to none.

The Public Economy Projectt (PEP), in the Southern Centre for Inequality Studies at the University of the Witwatersrand, gave its prognosis of the country’s economic predicament ahead of next week’s budget.

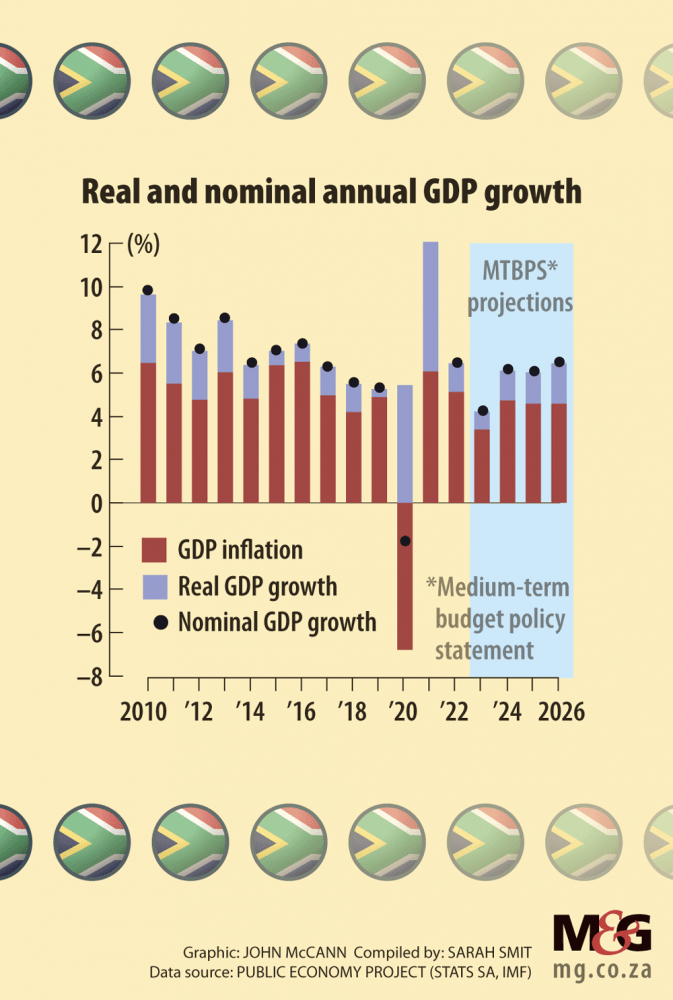

The project, led by former treasury official Michael Sachs, noted that in the aftermath of the 2008 global financial crisis South Africa’s economy has stagnated, resulting in declining real per capita income over the past 12 years.

Graphics: John McCann/M&G

Graphics: John McCann/M&G

This economic malaise coincided with the treasury’s policy of fiscal consolidation, administered from 2012 in an effort to stabilise public debt by cutting spending. This consolidation had a deleterious effect on the economy’s ability to grow, according to the PEP. Moreover, treasury’s cost-cutting attempts ended up having a limited effect on stabilising the sovereign’s debt. Gross loan debt increased from 23% of GDP in 2008 to 71% in 2022.

Following the more positive outlook the year before, in February 2023 the treasury was somehow even more optimistic, indicating that the government would achieve a primary surplus (when revenue exceeds non-interest expenditure) a year ahead of schedule.

But the economy’s prospects quickly deteriorated. Load-shedding intensified, causing the economy to grow by only 0.3% in the first nine months of the year. Interest rates soared, adding pressure on the economy, as well as government finances.

In the wake of much higher debt servicing costs, a larger-than-budgeted public sector wage bill, other overspending and lower tax collections, the treasury again finds itself nearing the edge of a fiscal cliff. Although some may consider this a self-created predicament, the treasury’s policy constrains the government’s ability to grow the economy.

Duma Gqubule, a research associate at the Social Policy Initiative, said next week’s budget will be a non-story insofar as economic stimulus is concerned. He suggested that the country’s crisis — which has seen it lag other emerging market economies — is an indictment of the ANC’s leadership, calling the party’s time at the helm “30 wasted years”.

But the country’s economic trajectory is probably best viewed as one of two halves, the 15 years leading up to the 2008 global financial crisis and its immediate aftermath and those that followed.

From 1994 to 2008, growth averaged 3.6%. While disappointing, this is higher than the average growth rate over the years that followed.

“Generally South Africans felt that things were improving. It wasn’t spectacular. But since the global financial crisis, the wheels have come off,” Gqubule said. The second period was marked by a collapse of public sector investment, in line with the treasury’s policy of fiscal consolidation after 2012, adding: “Until we start spending again, on our people and infrastructure, everything will continue collapsing in South Africa.”

But a more orthodox view of macroeconomic policy dictates that, in the context of soaring debt costs, the state should abstain from spending to avoid a full-blown fiscal crisis.

Kevin Lings, the chief economist at Stanlib, said South Africa’s economy probably won’t register any substantial growth anytime soon. “For that you need a catalyst. You need something that gets it better. And what is that something going to be? There is nothing really,” he said.

Lings forecast growth of about 1% in 2024, which while marking an improvement on last year’s meagre expansion, is still very low. “It’s certainly not going to make a helluva big difference. The population grows at about 1.6%, so that’s kind of your starting point. You really need to beat the population growth rate in any economy, especially in an economy with high unemployment.”

According to Lings, this catalyst won’t come about through fiscal policy. He noted that the traditional levers to stimulate the economy — tax cuts and expanded spending — are out of the treasury’s reach.

“That is going to be difficult to stomach in the short term, because the government — certainly the minister of finance — is trying to reflect a consolidation of debt levels,” he said.

“If you cut taxes, you’re driving consumption. You’re not necessarily driving investment and employment … And when that stimulus runs out, you’re back to where you were. It’s a bit of a sugar rush, but you are not going to get sustainability.”

The government would also want to avoid taking on more debt to fund new infrastructure spending given that borrowing costs are so high, Lings added.

In the absence of fiscal measures, the government has focused its policy efforts on structural reforms, viewed as a way of improving the supply side of the economy by removing institutional and regulatory brakes on markets.

But these reforms take time to bear fruit — and there is little consensus on just how much economic growth they will end up delivering.

In 2019, Asghar Adelzadeh, the director and chief economic modeller at Applied Development Research Solutions, compared a number of policy scenarios, assessing their potential to induce growth and create jobs.

The so-called microeconomic policy reform scenario — based on a view championed by the treasury that lifting supply-side constraints would stimulate the economy — yielded disappointing results.

According to Adelzadeh’s report, this policy scenario would add only 0.3% to the average annual growth rate. This limited payoff suggests structural reforms need to be implemented alongside macroeconomic measures, such as increased public investment, to induce significant economic and employment growth.

This week, Adelzadeh pointed to the post-pandemic economic trajectory in the United States, where at 3.7% unemployment is running well below the long-term average of 5.7%. “During the Covid crisis, unemployment reached about 15% and has been brought down to 3.7%. In South Africa, the official unemployment rate reached 35% and has come down to about 32%. That is all that has been achieved,” he said.

America’s post-Covid employment growth is largely attributed to fiscal stimulus employed by President Joe Biden’s administration to buoy the economy through the crisis.

“The role of fiscal policy is very important,” Adelzadeh said, adding that the conservative approach to macroeconomic policy is a consequence of ideology.

Although fiscal policy was once widely used by governments to stimulate employment, this became difficult when exchange controls — restrictions on currency outflows — were relaxed after the rise of monetarism in the late 1970s. Monetarism considers changes in money supply as the most significant driver of economic growth.

In South Africa, the Growth, Employment and Redistribution strategy, widely regarded as having failed to deliver on its core priorities, focused on the removal of exchange controls, among other things.

Adelzadeh said the post-1994 macroeconomic strategy had two main aims: avoiding permanent increases in the overall tax burden and eliminating deficit spending. These have constrained government investments in infrastructure, thus deferring their economic growth and employment benefits.

“Every year at this time the chief economists of all the banks and others who support staying the course, line up behind the treasury to say … ‘There are some green shoots. We’re turning a corner, so just stay put.’ That has been going on for many years,” he said.