On the money: Treasury director general Duncan Pieterse says its focus is on Transnet’s turnaround plan. Photo: Jaco Marais/Gallo Images via Getty

Explaining the government’s new, no-nonsense stance on state-owned entities, treasury director general Duncan Pieterse said there were no plans to grant Transnet a bailout.

At the time of his medium-term budget policy statement in November, Finance Minister Enoch Godongwana seemed to leave the door open for a bailout. But that door appears to have been firmly closed with the treasury’s decision to grant the beleaguered ports and rail utility a R47 billion guarantee facility the following month.

“We have no intention of giving Transnet a bailout,” Pieterse said in an interview on Wednesday evening.

Godongwana delivered his budget speech — which made little mention of the state-owned entity — earlier that day.

“Transnet has a guarantee and associated with that guarantee is a turnaround plan, which they produced. Our job is to support them to execute that turnaround plan.

“If they execute that turnaround plan, it’s not necessarily the case that they will need a bailout, because that turnaround plan is meant to bring them to financial sustainability. And that’s our focus,” Pieterse added.

The decision not to bail out Transnet — which has a debt pile in the region of R130 billion — comes as the entity’s decline continues to inflict pain on the country’s mining industry, which faces a wave of retrenchments as it also reels from sharply lower commodity prices.

Strings attached

In the same vein as the debt relief granted to Eskom, Transnet’s guarantee facility comes with strict conditions, which the treasury reported to parliament last week.

According to the budget document, these conditions require Transnet to divest non-core assets, reduce its cost structure and explore alternative funding models for infrastructure and maintenance.

Eskom has already had a taste of what happens when it fails to comply with the government’s strict conditions.

The budget document revealed that Eskom’s relief payouts would be cut by R4 billion after the power utility failed to dispose of its finance company. The cuts will be administered through two R2 billion reductions on Eskom’s 2023-24 and 2024-25 allocations, initially set at R78 billion and R66 billion, respectively.

The R4 billion might be considered small change, given that the total debt takeover was initially set at north of a quarter trillion rand.

But the treasury has set out other measures through which to penalise Eskom, should it continue to step out of line.

This includes converting the loan to the utility from being interest-free to interest-bearing for as long as it fails to meet its conditions.

“It’s about introducing much more discipline into the kind of support to state-owned companies that they get from the fiscal framework in response to the requests that we’ve received,” Pieterse said on Wednesday, later adding that this marks a significant divergence from the past practice of doling out “bailouts and guarantees without any enforceable conditions”.

The treasury has good reason to enforce these conditions, given that they are central to the government’s efforts to get South Africa’s laggard economy to finally grow.

According to the treasury’s forecast, the country’s GDP will grow at an average of 1.6% over the next three years — which, although better than previous predictions, is not enough to inspire substantial job creation.

The budget document sets out the government’s plans to “catalyse” growth through structural reforms, noting that South Africa’s economic prospects are highly dependent on well-functioning network industries, such as energy and logistics.

Among the mentioned reforms is the so-called freight logistics roadmap, which the cabinet approved in December. The roadmap is the basis for the conditions on Transnet’s guarantee facility.

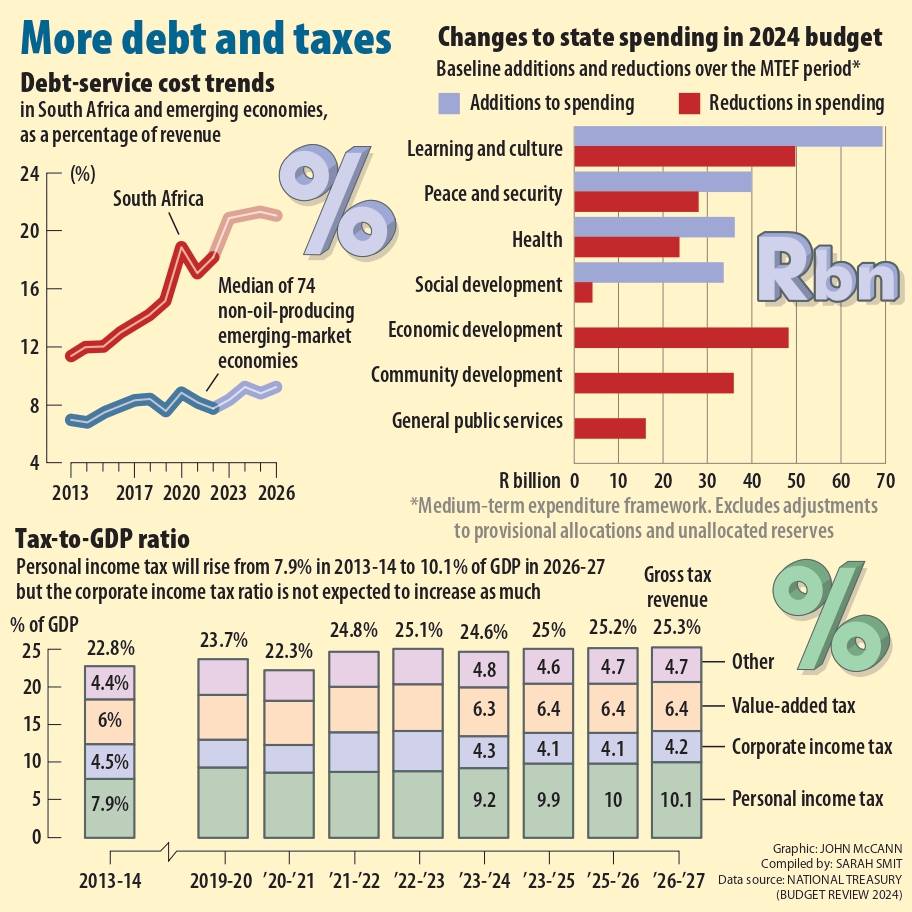

(Graphic: John McCann/M&G)

(Graphic: John McCann/M&G)

Treading carefully

Asked whether a measure to enforce reforms on state-owned entities constitutes overreach on the treasury’s part, Pieterse said: “You can’t on the one hand say that the national treasury is not doing enough to ensure that its contingent liability portfolio [guarantees] are being effectively deployed at no risk to the taxpayer and also say that the national treasury is interfering in the affairs [of state-owned entities].

“Anyone who comes for support from the fiscal framework — in particular those entities that are not meant to get support from the fiscal framework, schedule two entities that are meant to be self-financing and self-sustaining — we have a responsibility to exercise on behalf of citizens and taxpayers to ensure that whatever support we give them translates into the right kind of operational efficiencies. Otherwise we wouldn’t be doing our job.”

That said, enforcing this compliance does involve something of a balancing act, to the extent that the government doesn’t want to end up hurting state-owned entities more than it helps them.

Referring to the treasury’s enforcement’s of Eskom’s relief conditions, Pieterse said: “There is a fine line between being tougher and denuding the debt relief programme so much that you unwind its benefit for the Eskom balance sheet and they have to come to you for a bailout anyway.”

Even if Eskom’s loan becomes interest-bearing, the treasury cannot charge it an exorbitant rate, because that would “defeat the purpose”, he added.

“So, there is always this fine balance to be had between how you strengthen accountability but not doing it in a way that forces the entity to come back to you for more debt relief or a bailout. And that balance is something we have to tread very carefully.”

Pieterse joined the treasury in 2013. The decade that followed was arguably the toughest time for the country’s public finances. The economy stagnated and interest rates on government debt increased, prompting the treasury to adopt a policy of fiscal consolidation.

Not a negotiating position

But the treasury has often been criticised for failing to follow through, its budgets coming across as negotiating positions instead of final offers as the government seemed to accede to political demands on the fiscus. The treasury’s tougher approach to state-owned entities suggests it is pushing back on this perception.

The budget tabled this week was Pieterse’s first as director general.

“I’ve tried to — and I have certainly had the minister’s support — make sure that budget is a credible reflection of our demands,” Pieterse said.

He noted, for example, that this year’s budget already takes into account President Cyril Ramaphosa’s promise to extend and improve the Covid-19 social relief of distress grant by making provisional allocations for it beyond the coming fiscal year.

“If we know that there is currently a social relief of distress grant in the system — and it is unclear when that will go away and what will replace it — the most credible thing to do is to have the social relief of distress grant in the fiscal framework,” Pieterse said.

“If you know that there is a wage agreement that has been signed and that wage agreement has to be provided for — especially for personnel-intensive departments that have no choice but to institute very severe cuts in order to afford it — what you have to do, in my view, to put forward, is cater for that wage agreement in its totality. That is what we have done.”

But Transnet is slightly different, according to Pieterse. “Because I don’t believe a Transnet bailout is inevitable. I think that Transnet themselves has put a very credible turnaround plan on the table.

“I think we have a national freight logistics roadmap that makes sense, that is cabinet-approved. And we have given them a guarantee. So, all in all, this budget certainly is not a negotiating position.”