Platinum producers have oversupplied the market to such an extent that, even if nothing was mined for an entire year, global demand would still be more than satisfied.

This has been the case for several years now, with the industry producing more than what the market requires. Analysts say the over-production is the result of overly optimistic predictions of demand for platinum, mainly used in the manufacture of autocatalysts, which date as far back as a decade ago.

But the forecasts have proved incorrect, and efficiencies such as recycling technologies have muted the need for new platinum production.

Still, platinum mining companies have continued to pile up the precious metal, meaning that the commodity price has been under pressure. Despite limited or no production from the major mining houses as the strike persisted over the past four months, the oversupply of platinum is so substantial that the metal price – staying around the level of $1 450 an ounce – has failed to respond notably to the developments.

This glut in the platinum market is now a significant factor, which has limited the ability of the platinum companies to negotiate wages. And although employees are standing firm on a demand for a R12 500 minimum wage, employers maintain that they simply cannot afford it.

Research by Michael Kavanagh, a metals and mining analyst at Noah Capital Markets, using data from speciality chemicals company Johnson Matthey, shows that platinum firms have flooded the market for 35 years, year after year, resulting in a cumulative surplus between 1975 and 2013 that exceeds seven million ounces – about a million ounces more than 2013 net demand.

Golden goose industry

According to Kavanagh, some still view platinum as a golden goose industry when it is actually more like a dying duck.

The industry thought demand would grow in response to new emissions regulations. Car component manufacturers would require more platinum, as it was expected more metal would be needed in the manufacture of an autocatalyst in order to adhere to emission standards.

According to Kavanagh, planning and building a platinum mine from the start until reaching full production could take anything from 10 to 20 years, and mining companies would have to forecast what demand might be.

“But auto-makers and catalyst-makers got clever and were able to use the same amount or even less,” said Kavanagh, noting that some substitutes such as palladium are also used in the manufacture of the device.

“Fortunately for them, they [the mines] never delivered [on] their production promises,” he said.

In its 2000 results presentation Anglo American Platinum announced it would increase platinum production to 3.5-million ounces, citing more stringent emission legislation as the driver of future demand, but by 2006 refined platinum production was only up to 2.8-million ounces. Its 2013 annual report showed it produced and sold 2.3-million ounces – “in line with strategy”.

‘Accelerated expansion plans’

Impala Platinum produced just over two-million ounces by 2006 and has since reduced gross refined platinum production down to 1.58-million ounces.

In 2000 Lonmin reached record production levels, reporting almost 660 000 refined troy ounces of platinum produced. The review noted “strong market fundamentals support accelerated expansion plans.” Yet in 2013 it reported platinum sales of just 696 000 ounces.

A decade ago producers also expected the development of hydrogen cell technology would spur demand, although it has not taken off as yet.

Peter Major, a mining analyst at Cadiz corporate solutions, said Anglo American Platinum, the world’s largest producer of the metal, went all in, expecting demand to surge. Major noted that many commodity markets go into oversupply at times.

“They thought: If you are the biggest you can control the price, they thought they were going to be an Opec,” Major said. “But then you end up in a situation where you have so much you can’t get out of it … It was a gross miscalculation on Amplats’ side … They lost control of it.”

Apart from overly optimistic demand forecasts, the transition in government in 1994 also brought with it a number of unexpected surprises.

Double-digit wage settlements

“The Nats [National Party] did understand a little bit about the market; they kept it tight. But when the new government came in they issued platinum mining licences all over,” Major explained.

The new administration also introduced a “use it or lose it” clause for mineral rights, forcing companies to develop. The introduction of economic empowerment also obliged companies to take on partners and develop mines more quickly.

“It didn’t work out as planned and I wonder how well they thought it through. Did they take into consideration the realities of the day?” Major asked, given that lower levels of productivity and double-digit wage settlements year after year were “a nightmare no one could have contemplated in the Nineties”.

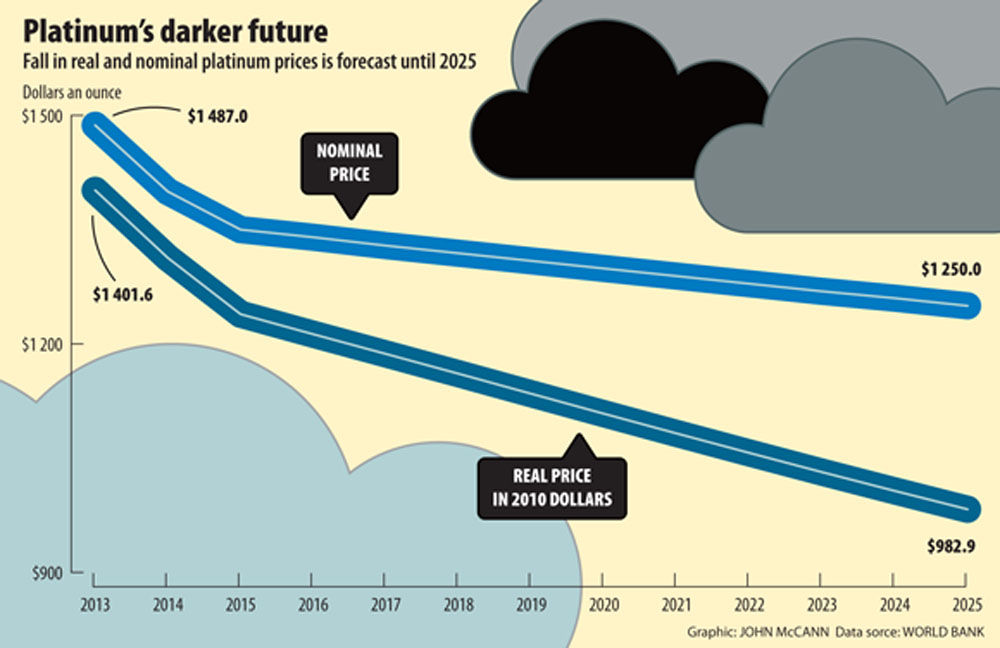

Although the price has not been pushed upward as a result of the labour action in the North West, it is said to be higher than it likely should be. A recent World Bank commodity markets outlook report forecasts the price to drop over the next decade before reaching $983 an ounce in 2025.

Despite the glut in supply, industry analysts say mining companies are forced to produce high volumes to keep unit costs down. “If you produce fewer ounces, the footprint doesn’t get less,” Kavanagh said.

Economic recession

Those who can produce more metal at a cheaper rate than others would theoretically push the smaller miners out, although this has failed to happen and now the entire industry faces decline, and even some of the largest in the business such as Anglo Platinum and Lonmin have suggested that restructuring may be on the cards if the strike cannot be resolved soon.

“[It’s] not like having a manufacturing line and just turning it off when demand declines,” one analyst who wished to remain anonymous explained. “For a mine it takes a long time, and it’s a very expensive decision to stop it.”

The economic recession brought with it an unpredictable drop in industrial demand that was “very material”, the analyst said. “The ability of companies to respond to something like that is very limited.”

South Africa’s labour legislation makes it difficult to stop production, the analyst said. “Guys have to have a real tough look at how to reverse the footprint. It’s a massive exercise.”

“They usually need to retain optionality; if there is a big demand then they can respond,” Kavanagh said, adding that considerations around optionality have been replaced with considerations of survival.

“As demand fails to grow, they don’t see the cash flows; it provides a natural handbrake on investment.”