Capitec chief executive Gerrie Fourie is confident the unsecured lender will prove Moody's wrong.

It wasn’t the failure of African Bank that prompted Moody’s to downgrade the ratings of South Africa’s big four banks, but rather the Reserve Bank’s innovative remedy that causes investors to share the burden with taxpayers.

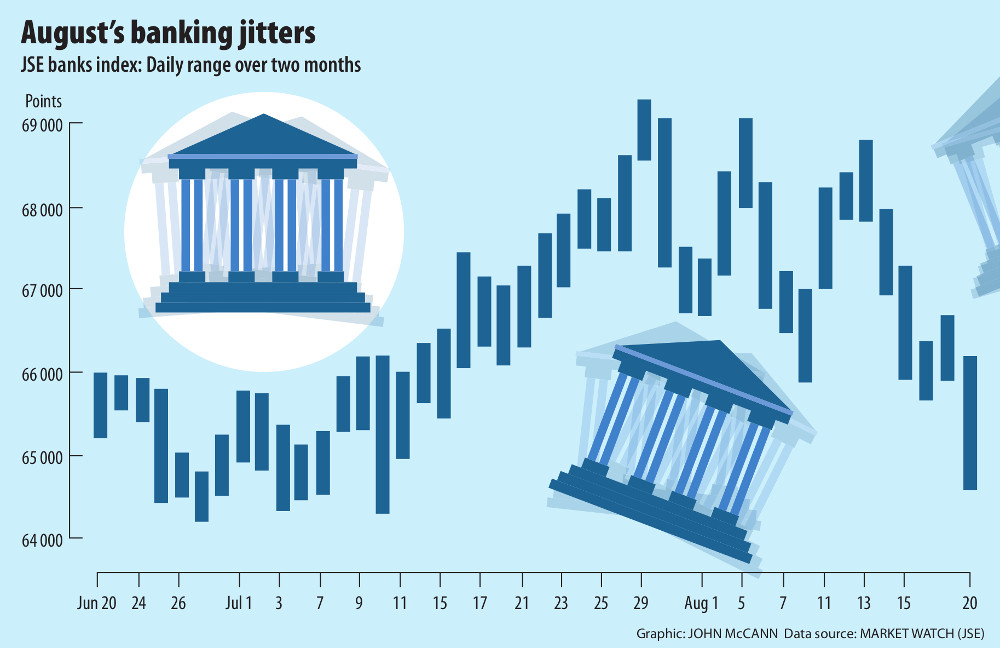

Taking the market by surprise, rating agency Moody’s revised the ratings of Standard Bank, Absa, First Rand and Nedbank down by one notch on Tuesday, which followed a double-notch downgrade of Capitec Bank at the weekend.

There were a number of reasons for the big four’s downgrade, including weak economic growth, consumer affordability and indebtedness. But the most prominent reason, which Moody’s indicated had prompted the timing of the updated opinion, was the Reserve Bank’s response to the abrupt loss of creditor confidence in African Bank.

“The policy response addressed related liquidity and capital issues, thereby mitigating contagion risks with the further objective of minimising potential losses,” Moody’s said in the announcement. “However, the inclusion of a bail-in of senior unsecured bondholders and wholesale depositors indicates the regulator’s willingness to impose losses on creditors.”

Whereas a bail-out refers to the use of public funds to rescue a firm, a bail-in uses private funds. The Economist, which first coined the term, described a bail-in as a situation in which the institution’s creditors are forced to bear some of the burden by having some of the debt written off.

The rescue measures included the recapitalisation of the bank through the Reserve Bank and, to some extent, by bondholders and wholesale depositors, who took a 10% haircut – the term used for the difference between the market value and the purchase price of an asset.

Burden-sharing

Sean Marion, an associate managing director at Moody’s, told the Mail & Guardian it is not solely a question of magnitude of losses but what the actions signal in terms of the direction towards burden-sharing of losses with investors.

“As we move out of the global financial crisis, governments are shifting their focus to protecting their balance sheets, and we have seen the global support environment evolving with legislations either being implemented or in the process of being implemented regarding the resolution process,” Marion said.

“These developments need to be reflected in our ratings as they are clearly credit-negative for creditors, and we have been reducing or removing support assumptions from our bank ratings in response to these developments.”

The move toward bail-ins is becoming widespread and it’s believed to have been bolstered by a 2012 International Monetary Fund staff discussion note, “From bail-out to bail-in: mandatory debt restructuring of systemic financial institutions”, which said that “too big to fail” financial institutions had become costly and even unaffordable for some sovereign states to bail out and this safeguard also risked increasing “moral hazard” (a lack of incentive to guard against risk).

The paper suggests one way to protect taxpayers is a bail-in: “A statutory power of a resolution authority to restructure the liabilities of a distressed financial institution by writing down its unsecured debt and/or converting it to equity.”

The statutory bail-in power is intended to achieve a prompt recapitalisation and restructuring of the distressed institution, the paper said.

Bail-in legislation

Although bail-in legislation is yet to be implemented in South Africa, the remedy applied to African Bank has laid some of the responsibility of halting a systemic failure at the feet of investors, in this case African Bank’s bondholders, but it also served to help them.

Jean Pierre Verster, an analyst at 36ONE Asset Management, said he believed the “bail-in” concern was not a valid justification for a downgrade because the bonds had been trading significantly lower before the bail-out news than they did after the bail-in. “So it has been a net positive for investors.”

Moody’s, he said, wanted to see those investors compensated, “but by doing that, the Reserve Bank would have been sending the wrong signal”.

The Reserve Bank publicly stated it did not agree with the decision, but Nomura analyst Peter Attard Montalto said the Reserve Bank’s statement missed the point. “The downgrades were because the Reserve Bank’s support was less than Moody’s had originally factored in. We think the senior debt bail-in is ultimately what triggered this view.” He noted, however, that the use of a bail-in was appropriate and that the Reserve Bank’s commitment to financial stability is unquestioned.

It does not appear likely that other ratings agencies will follow suit.

Dependent on support

Redmond Ramsdale, director of financial institutions at Fitch Ratings, said the agency viewed a bail-in as neither a positive nor a negative but that it rather “depended on how much support was built into the rating”.

“The Reserve Bank will assess each situation on its own merit and come up with its own solution for each situation. What happened last week with African Bank we see as an isolated incident. We don’t see it as putting pressure on our ratings.”

The bigger driver of a ratings downgrade would be a deteriorating operating environment and weakening gross domestic product, Ramsdale said.

Standard and Poor’s said it has no plans to downgrade South African banks because the rescue plan was in line with global best practice.

But the biggest question mark hangs above Capitec, said Verster, noting that, although it was logical to look at Capitec because it did a great deal of unsecured lending, it was “dubious” to downgrade it “on the back of a half-hour conversation over the phone” and just two months before its results are released.

Charm offensive

Capitec chief executive Gerrie Fourie is confident that the unsecured lender will prove Moody’s wrong. Its unexpected two-notch downgrade put Capitec on a charm offensive this week, as it worked hard to assure investors as well as its customers that it was a very different institution from African Bank.

Capitec, and a number of market analysts, viewed Moody’s decision as a reaction to African Bank’s plummet and subsequent rescue by the Reserve Bank. The latter said it did “not agree with the rationale” given by Moody’s.

Capitec was well capitalised, Fourie said this week, and would not need funding for the next 18 to 24 months. For now the downgrade had had little immediate effect on its cost of borrowing.

“We have enough time to prove Moody’s wrong … and we assume in the next three to four months they will come do a re-rating and one will have to see what comes out of it.”

Capitec is due to announce its results on September 29, and so far “everything is in line with budget”, said Fourie.

Capitec, like African Bank, focuses on unsecured lending, primarily to low-income earners, but it stressed some key differences between the companies — including its more diversified business model. African Bank, which held almost no deposits, relied chiefly on wholesale funding to finance its lending to borrowers with no collateral.

Better insight

Capitec had a “well-balanced” mix of wholesale and retail funding, with 67% of its funding requirements from retail sources. It had a banking relationship with its 2.3-million retail clients, giving it far better insight into their income streams and their credit bureau information, said Fourie.

But poor economic growth, rising inflation, higher living costs and strikes have weighed on consumers, particularly low-income earners. Fourie said Capitec was carefully managing its affordability criteria and credit models, and making adjustments where necessary.

“If you take a look at credit policies in these types of economic situations, it’s like everywhere … When it’s going well banks tend to give credit more easily and when it’s tight then they pull back,” said Fourie.

Fourie argued, however, that the economy needed clear direction and implementation of the government’s National Development Plan, which is aimed at addressing South Africa’s levels of inequality and unemployment.

Analysts this week supported the view that Capitec was not the same as African Bank, with Attard Montalto calling it a “very different beast”.

Apart from better provisioning and funding, there were “a wider range of business lines and a much more risk-adverse loan extension and risk management practice”, he said in a research note.

Montalto also pointed to the fact that African Bank was weighed down by its ill-fated purchase of furniture business Ellerines.

“They [are] exposed to the risky unsecured debt market, obviously, but the way they have handled it is very different from [African Bank] and means they are still not a systemic risk through their debt or through deposits, given the provisioning policies already in place,” he said.