The government has introduced tax-free investment regulations in a bid to boost household savings.

Financial institutions have scrambled to provide the most attractive tax-free savings, ranging from simple bank deposits to investments exposed to the stock markets.

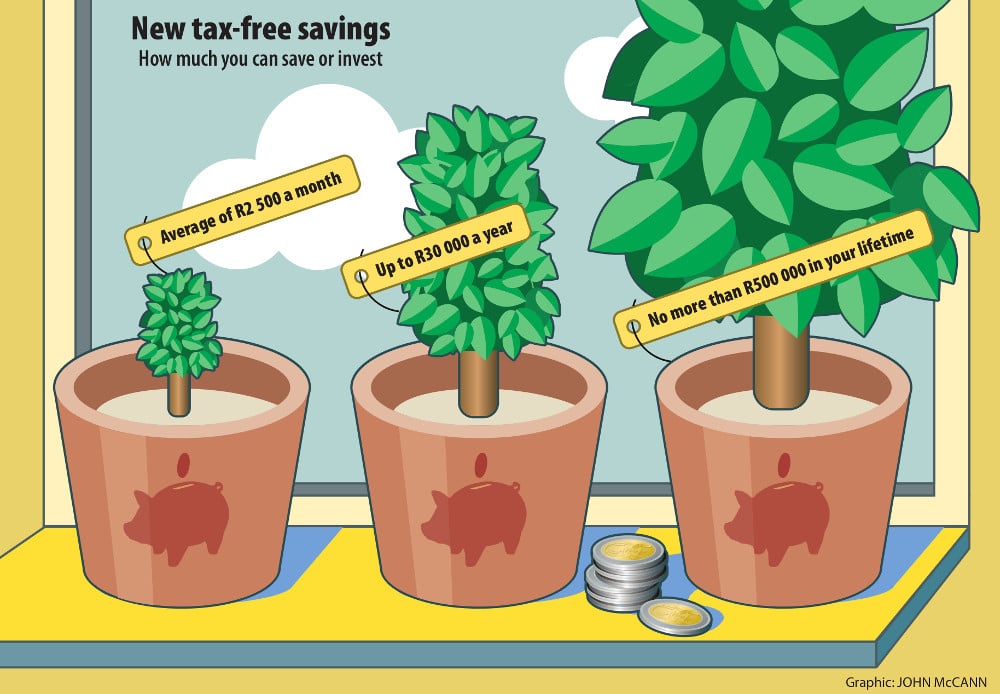

At the beginning of this month, the government introduced tax-free investment regulations in a bid to boost household savings. Regardless of what form the tax-exempt investment takes, the regulations allow for amounts of up to R30 000 a year (an average of R2 500 a month) and no more than R500 000 over a lifetime.

If investors exceed the contribution limit, they will be subject to a 40% tax on the investment. Interest earned on the amounts is not considered as contributions.

The regulations require that new special products must be used to gain the tax-free benefit. Existing accounts do not apply.

If the tax-free investment has a maturity date, the regulations require that it must be paid up within 32 business days. If there is no maturity date, such as a savings account, it must be paid on request within seven days.

Account limitations

Tax-free savings products cannot be used like accounts, and so services such as debit orders or ATM withdrawals are not allowed. Once a tax-free investment has been opened, the funds in it cannot be transferred to another tax-free fund before March?1 2016.

The accounts are not necessarily exempt from fees although the regulation requires these “must be reasonable”.

Many of the funds offered by financial institutions stipulate minimum monthly contributions, but the regulations say investors cannot be charged a fee for not paying those amounts, paying less or ceasing payments.

Of the big five banks, three have launched special products.

Nedbank’s tax-free savings account requires a minimum R50 deposit and the account can attract interest rates of up to 5.25%. Partial withdrawals can be made if they exceed R50 and a minimum of 24 hours’ notice must be provided. There are no fees or commissions, but the bank reserves the right to charge a fee for cash deposits exceeding R5 000 in any calendar month.

Deposit accounts

FNB’s tax-free cash deposit account requires a minimum investment of R1 000. Customers must give 32 days’ notice to make a withdrawal. In extreme circumstances, the bank will consider shorter notice periods, but there will be a charge. Interest can be up to 6.15%, but it cannot be reinvested or redirected to another account.

Standard Bank has launched a tax-free call deposit account, which pays interest of up to an effective 5.48% and requires a minimum deposit of R250. The interest can be reinvested monthly or paid to another account. Funds can be made available within seven days but withdrawals and transfers between accounts attract fees. Research by the bank shows that regular annual contributions of R30 000 into this account will result in a gain of R319 000 by year 17, assuming rates stay the same and, with the interest earned daily and capitalised monthly, amounting to a total balance of about R819 000.

Investec also offers a tax-free fixed deposit account with an attractive rate of 7% annually. But it requires a lump sum investment of R30 000 for 12 months for it to guarantee the fixed rate. The minimum withdrawal amount is R5 000 and is subject to fees.

Capitec said it is working on a product that will benefit low-income earners in particular, but noted that its current longer fixed-term saving products offer a higher interest rate (up to 9.25%) than what the rest of the market offers on tax-free cash-on-call accounts, including their tax benefits.

Absa said it is about to launch a tax-free savings product but would not provide further details.

Stock exchange

Experts say long-term investors are likely to want exposure to shares in order to beat inflation, and the tax-free investment legislation allows individuals to invest in the stock exchange without paying the taxes normally associated with these, such as dividends tax, which is 15%. The same contribution limits apply to these investments, and may be subject to brokerage fees and permissible charges.

Some of these vehicles include Old Mutual’s tax-free plan, which allows customers to invest in several funds, including those exposed to equities. It requires a minimum monthly investment of R350, or R1 050 a quarter, R2 100 half-yearly or R4 200 a year. Investments can also have access to external funds, such as Prudential or Coronation, but only if a financial adviser is used. This attracts an advice fee. Withdrawals can be made at no charge and funds will be paid out within seven days.

SBG Securities offers a product in which you can select from listed securities, with a minimum of R250 for each share a month. Left-over cash or dividends will be kept in the account for reinvestment. The proceeds from selling shares will be made available within five business days.

There is a brokerage fee of 0.25% and statutory charges can be as much as R98 a month, depending on the value of the investment. There is also a monthly fee of R10.

FNB’s tax-free shares account allows existing customers to invest in the top 100 companies on the JSE and investments begin from R300 a month or a R1 000 once-off lump sum. These investments attract fees of 0.4% (plus value added tax) a year.

Unit trusts

Sanlam offers two options: a tax-free unit trust, which allows consumers to choose investment funds, from R500 a month; and the Satrix tax-free unit trust, which offers low-cost access to a lifetime investment option from R300 a month. Satrix, the investment platform wholly owned by Sanlam, also provides tax-free unit trust and exchange traded-fund options, to which the same minimum deposits apply.

Karin Muller, the head of growth market solutions at Sanlam, said some people would use tax-free savings accounts more than others. “Like in the middle-income market, it can be used for savings toward education. It is a better vehicle than some of the endowments, although it is limited in how much you can contribute.”

But using tax-exempt accounts as a short-term investment did not take full advantage of the tax benefit, Muller said. The real benefit would only occur after the maximum contribution was paid, according to Sanlam’s calculations. If the full R30 000 was paid consistently each year, this would take 16 years and eight months. “The real additional savings only come if you are invested after that,” she said, because of compound interest.

Daniel Wessels, a financial adviser at Martin Eksteen Jordaan Wessels, said, because tax-free account contributions were limited, ideally they should not replace a retirement annuity (RA), which is also tax exempt.

Tax-free savings contributions are made from money that has already been taxed, but they are exempt from tax thereafter. RA contributions are exempted from tax, but the returns, when withdrawn, are taxed.

Retirement annuities

Wessels said retirement annuities had benefits a tax-free account didn’t. “The real benefits of an RA are not always quantifiable. For example, it is protected from creditors. This week, I had someone here who was insolvent but still has his RA.” He said RAs were also exempt from estate duty and were less liquid – you couldn’t cash them in until you were 55.

“Tax-free investments should become a mainstream investment vehicle, to replace ordinary investments, especially for younger people. You can’t lose with this investment … it’s a no-brainer.”

But there was no single ideal option for every saver, he said. Ultimately the vehicle chosen depended on the amount invested, the period and the goals of the investor.