Off target: Capitec Bank took on short-seller Viceroy, whose founder Fraser Perring is pictured, and whose report on the bank was subsequently found to be false. (Photo: Guillem Sartorio/Bloomberg via Getty Images)

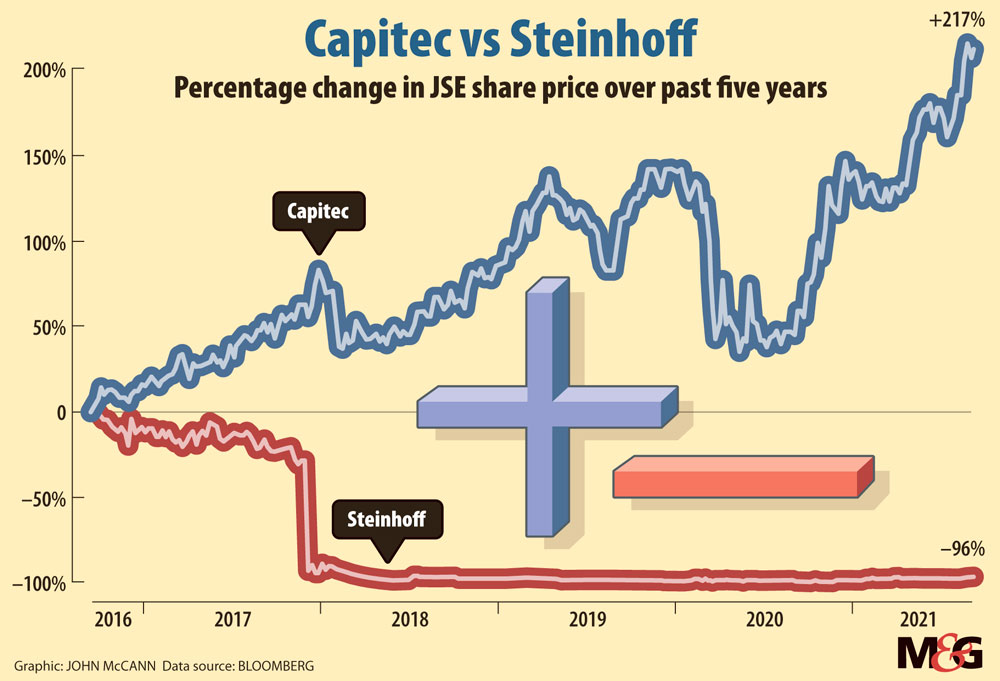

When US short seller Viceroy took aim at Capitec at the start of 2018, the bank had grown its client base by 83% in five years and was in the middle of a strong run on the JSE. Being labelled a loan shark hit Capitec’s share price, but not for long — and the bank’s stock has risen 86% since Viceroy pinned its hopes on a fall from grace.

In January 2018, Viceroy released an explosive report titled Capitec: A Wolf in Sheep’s Clothing, which accused the bank of engaging in predatory lending and of having a loan book that was “massively overstated”.

The report caused Capitec’s share price to immediately plummet 23.12%. But the bank, which came onto the scene in 2001 to take on South Africa’s long-toothed big four, recovered quickly. And in the years since, it has continued to prove its mettle, analysts say.

Last week, the Financial Sector Conduct Authority (FSCA) announced that it had fined Viceroy R50-million for publishing false and misleading statements about Capitec.

This week, Capitec said it had noted the authority’s ruling, but added it has no further comment as the matter “is entirely between Viceroy and its partners and the FSCA”.

Viceroy said it was appealing the FSCA’s decision because the authority’s grievances “were not based on an investigation into Viceroy’s claims, but into Viceroy itself, from the onset”.

“Based on the investigation conducted, the FCSA avoided placing Capitec under any scrutiny,” the short-seller added.

Fraser Perring, founder of Viceroy Research. (Photo: Christopher Goodney/Bloomberg via Getty Images)

Fraser Perring, founder of Viceroy Research. (Photo: Christopher Goodney/Bloomberg via Getty Images)

“When reading the FSCA report presented to the tribunal, you would be left wondering if Capitec were a grade A credit reference agency, rather than the most expensive deposit-taking institution in the world whose loan book is almost exclusively unsecured loans to financially vulnerable demographics.”

Shorting is when an investor borrows stocks, sells the stock and then buys it back to return it to the lender. The main point is to benefit from a falling share price. Short-sellers are betting that the stock they sell will drop in price.

“Viceroy went out with a bearish view on Capitec, published that view and probably had a short position. This is broadly how the industry works,” analyst and trader Simon Brown explained.

The Steinhoff spinoff

Viceroy’s 33-page report cast doubt on Capitec’s independence, noting that its board had links to disgraced retail firm Steinhoff — which the short-seller had been right about just a month earlier. “While this is not overly suspicious, we are cautious of incestuous management between these firms given Steinhoff’s poor corporate governance,” the report read.

The short-seller’s report on Steinhoff was released the day after the retail firm announced that its then chief executive Markus Jooste and its auditors Deloitte had refused to sign off on its financial statements.

On 5 December 2017, Jooste suddenly resigned from the helm of Steinhoff amid an investigation into accounting irregularities at the firm. Steinhoff’s share price plunged by more than 95%.

The Steinhoff report brought Viceroy into the attention of the market, Brown said, adding: “Steinhoff had been a well-loved company before that and then collapsed in a heap of accusations of fraud … If you make a really big, bold call and it turns out to be totally spot on, and you make a fortune from it, that does add to your status. And you will try and leverage that.”

In response to the FSCA’s findings, Viceroy questioned why similar action had not been taken against Steinhoff’s critics.

“The FSCA has proceeded to insult the public further by claiming: ‘We’re going to hold you liable for saying things, even on your personal blog. If that personal blog is on the public domain and those statements are negligent, we are going to come and hold you accountable.’ If this were actually the case, we would like to know how many fines have been issued to Steinhoff analysts who had jockeyed the company’s share price for years in the midst of obvious fraud.”

The not-so-big short

After its Steinhoff triumph, Viceroy revealed it had another South African company in its sights and the axe fell on Capitec. But, unlike the Steinhoff case, the knock to the bank’s share price and reputation was short-lived.

A Capitec spokesperson told the Mail & Guardian that the bank managed to avoid any lasting reputational harm resulting from the report by doing “everything possible at the time to clear our name”.

“We communicated with the market and made sure all the stakeholders had the correct information,” the spokesperson added.

At the time, Capitec’s largest shareholder, the PSG group, said “the Viceroy report is on the face of it filled with factual errors and misleading information”.

In a shareholder announcement, PSG added that the report triggered “unwarranted market turmoil”.

In its report, Viceroy said it believed Capitec should meet the same fate as African Bank and be put under curatorship by the South African Reserve Bank. But the central bank responded, saying Capitec was solvent and well capitalised.

Brown, who owns shares in Capitec, agreed that the bank responded well to the scandal.

“Most investors in Capitec … were aware of the issues that Viceroy had raised and didn’t consider them to be fraud, or as posing a material risk to the health of the business,” he said.

Companies can build a sort of immunity to shorting, Brown said. “A stock that just keeps on rising, has a great story to tell and has, for want of a better phrase, a fan club of investors, shorting it is high risk.

“And even if you are right, you have got to cut through the existing noise and enthusiasm for the company.”

Too big to fail

Compared to its competitors, Capitec’s share price has shown impressive growth, having risen almost 214% in the last five years. Standard Bank’s share price has only grown 6.56% in the same period and Absa’s by 3.7%. Nedbank’s share price has tumbled 17.41% in the last five years.

According to Intellidex senior banks analyst Nolwandle Mthombeni, Capitec’s growth rate sets it apart from its competitors. “They have been winning clients and they have been growing earnings in the high double digits …

“They have been winning market share for a long period of time, as opposed to over one or two years. They have been doing it consistently.”

Capitec’s growth may eventually slow down, Mthombeni added. The bank now has other digitally led competitors in Discovery Bank and TymeBank — which earlier this year declared itself “one of the world’s fastest-growing digital banks”, after bringing on board three-million customers in only 25 months.

But a slowdown in growth does not necessarily mean Capitec will be losing ground, Mthombeni said.

“The rate of how it slows down will depend very much on competition, but they are still far ahead in many respects. So I think they can sustain growth for a little bit longer, before they start losing.”

[/membership]