The rand has managed to withstand even the strongest global headwinds, but it is unlikely it will continue to hold steady in the wake of the Fed’s aggression. (Photographer: Waldo Swiegers/Bloomberg via Getty Images)

Despite the US Federal Reserve’s decision to step in this week — by hiking rates more aggressively than it previously envisioned — inflation looks to be beyond the point of return.

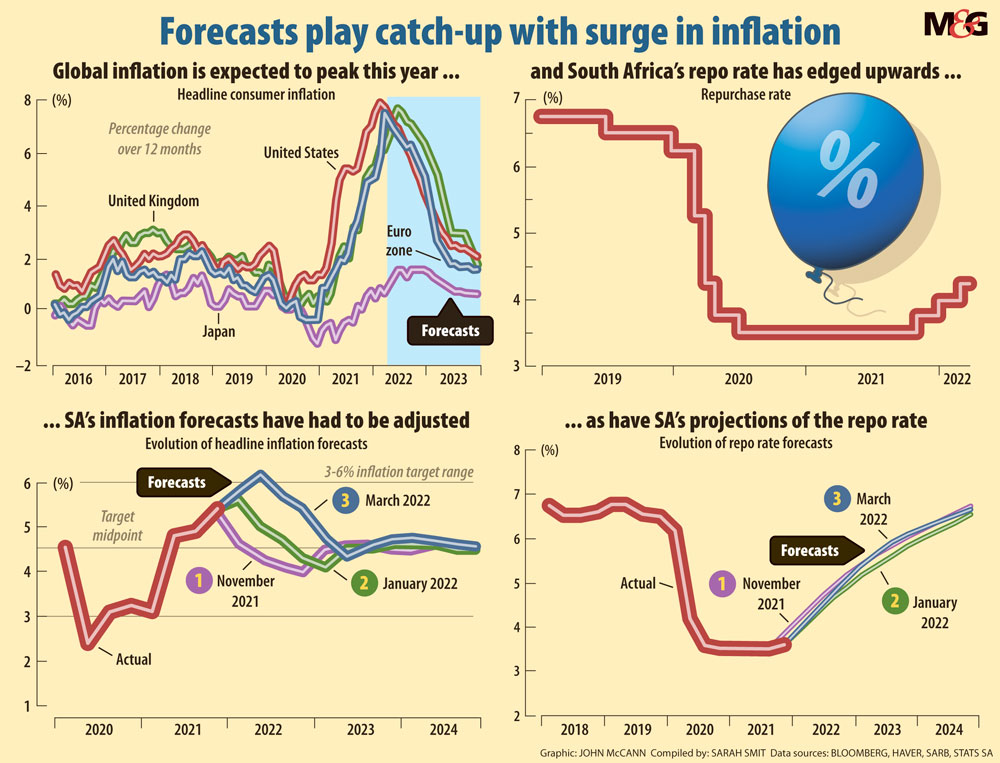

In South Africa, the outlook hasn’t appeared quite as dire: Since the start of the Covid-19 pandemic, consumer price inflation has kept within the South African Reserve Bank’s target range, a welcome symptom of the country’s less spirited economic rebound. The rand has also managed to withstand even the strongest global headwinds.

Recent weeks have proven that even more uncertainty lies ahead for South Africa’s currency. A resilient rand could carry consumers through inflation’s perfect storm. Analysts say, however, that the domestic unit will likely prove to be a cold comfort.

The rand has weakened 9% since mid-April. In late April, the International Monetary Fund (IMF) warned that inflation was looking to be far more stubborn than central banks once anticipated. All eyes turned to the Federal Reserve, which for the majority of last year took a dovish stance against elevated prices.

‘It was the perfect storm’

In 2021, inflation began its climb as the global economy roused from its Covid-induced slump. As demand ramped up, suppliers failed to keep pace in the wake of logistical breakdowns.

During this period, many central banks maintained that supply-chain chokeholds would subside and that inflation would be transitory. But Russia’s invasion of Ukraine — and a strict lockdown in China — proved that inflation’s path would be far more unpredictable.

At the IMF’s spring meetings, Fed chair Jerome Powell made a hawkish pivot, noting that a more aggressive rates hike would be on the table in May. Inflation in the US accelerated to 8.5% in March, the highest rate in 40 years. Powell’s pronouncement came to bear on Wednesday, when the federal open market committee decided to raise the federal rate by 50 basis points.

The Fed has been widely criticised for failing to quell inflation sooner, though — as Michael Power, a strategist at NinetyOne asset management, points out — its current dilemma isn’t entirely of its own making.

The large amounts of stimulus that the White House injected into the US economy caused its best performance since 1984. Supply simply could not keep up a far too vigorous rebound and the Russia-Ukraine conflict added to inflation woes by driving up energy and food prices.

“It was the perfect storm. However, I am not going to them off the hook for the fact that they sailed into a perfect storm. To some extent they should have seen at least some of it coming,” Power said.

The Fed now risks sending the US into a recession. Just a week after the IMF warned that global growth would stagnate in the coming years, GDP figures revealed that the US economy contracted by an annual rate of 1.4%. Higher interest rates now could worsen the US economy’s prospects.

“They are in a race against time. They are behind the curve. They have got to raise rates. They’ve got to cool things down. That’s the only way, ultimately, that a central bank can cool down the inflation rate,” Power said.

“But at the same time, it has to recognise that there is another consideration. And that is, that they can go ahead and raise rates, but crash the economy … The US Federal Reserve at the moment is on a knife’s edge.”

The Fed’s efforts to play catch up to bring inflation to heel means a period of concerted policy tightening is now upon us. In South Africa, the attention will be on how the Reserve Bank will react, as it endeavours to guard the value of the rand against financial market volatility. A weaker currency can trigger higher inflation by driving up the prices of imported goods.

The Reserve Bank began lifting the repo rate by 25 basis point increments last November amid signals that Fed officials were starting to get hot under the collar. The hike was the first since the bank slashed the repo rate, which affects the cost of borrowing, by 300 basis points in 2020.

Will the rand show its muscle?

At the time of the Reserve Bank’s decision, the rand had depreciated 5.9% against the US dollar over the span of two months. In the months following the hike, the local currency began to strengthen. By the end of March, it was trading at its best price since October 2021, even in the face of the war-induced shock to the global economy.

It is difficult to say whether the Reserve Bank will match the Fed’s inflation offensive. South Africa’s economy is currently facing the double threat of inflation and slowing growth — the result of yet another bout of load-shedding and the aftermath of the flooding that devastated KwaZulu-Natal last month. These two headaches have different remedies: Much higher interest rates will temper high prices, but they will likely do the same for growth.

The oil price has also moderated significantly since the Reserve Bank’s monetary policy committee last met in March. The lower oil price, as well as the temporary cut to the general fuel levy for April and May, will have soothed the pressure of fuel inflation on South African consumers.

But the rand’s recent tumble, and its effect on domestic inflation, will still weigh on the committee’s decision.

As Investec chief economist Annabel Bishop points out, financial markets have factored in three more 50 basis point hikes by the Fed before the end of the year, resulting in a 2% lift. In South Africa, forecasters are expecting a repo rate hike of just under 2% this year. A lower hike compared to the Fed would narrow the differential between South Africa and US interest rates, which typically results in a weaker rand.

But the rand will likely still benefit from elevated commodity prices, which shot up in the wake of Russia’s assault on Ukraine. Though they have now started to moderate, Momentum economist Sanisha Packirisamy noted that South Africa still has favourable terms of trade.

“Unless we get to a very negative risk-off event for a prolonged period of time, we would not expect that the rand will weaken significantly from its current level. We think that commodity prices will continue to keep the currency stronger, notwithstanding this recent bout of weakness,” Packirisamy said.

A bad predicament

Packirisamy said it is unlikely that the Reserve Bank will pivot from a gradual hiking cycle to an aggressive one, given the fact that inflation has not yet breached the 3% to 6% target range.

Inflation is currently just a hair’s breadth away from the bank’s ceiling, coming in at 5.9% in March. The Reserve Bank’s monetary policy review, which has signalled a “less transitory” inflation environment, forecasts that inflation will rise past the bank’s upper limit in the second quarter of 2022 before returning to the 4.5% midpoint next year.

Given the rand’s volatility, it is difficult to predict what the currency will do in the short term. However, in the long term, the domestic unit is bound to weaken, Alexander Forbes chief economist Isaah Mhlanga said.

The rand could strengthen if there is a shift in global sentiment. But this is unlikely. The only chance the currency has of strengthening significantly is if commodity prices shoot up again and if the Reserve Bank decides to hike rates aggressively, Mhlanga said. “Those are really the only two things that are supporting the currency.”

Mhlanga is not convinced that South Africans will reap the benefits of a stronger rand, which would cushion consumers against the worst of inflation.

Even if the rand does prove its resilience over the coming period, Michael Power said, “it will only serve us less badly”. The IMF has forecast that inflation in emerging and developing economies will average 8.7% in 2022.

“But again, we can’t live in a positive world of a currency serving us well. It serves us less badly than it does, for instance, Egypt or Sri Lanka or Tunisia. Those countries are in a far worse predicament than we are.”

[/membership]