The Constitutional Court will rule on whether parliament acted lawfully when it rejected a Section 89 panel report recommending an impeachment inquiry into President Cyril Ramaphosa over the Phala Phala scandal

When the country was gripped by the Covid-19 pandemic in 2020, members of organised business rallied to beef up the government’s efforts to avoid total disaster, mobilising resources through the Solidarity Fund and later helping to roll out the national vaccination programme.

Two years into Cyril Ramaphosa’s presidency — which, following the economic decline under the previous administration, was met with goodwill from the business fraternity — the private sector and the government had finally proven they could work together. This period sprung the Economic Reconstruction and Recovery Plan, aimed at setting South Africa back on the path towards growth.

Three years later, however, South Africa’s economy is barely better off than it was before the pandemic, its growth hamstrung by, among other factors, crumbling electricity and logistics infrastructure.

In recent months, Ramaphosa’s government and the private sector have recommitted to working hand-in-hand to fix the economy — but only after things became a lot worse. After losing one another in the wake of the pandemic effort, the two parties seem to have found common ground. But is it too late to secure Ramaphosa’s future?

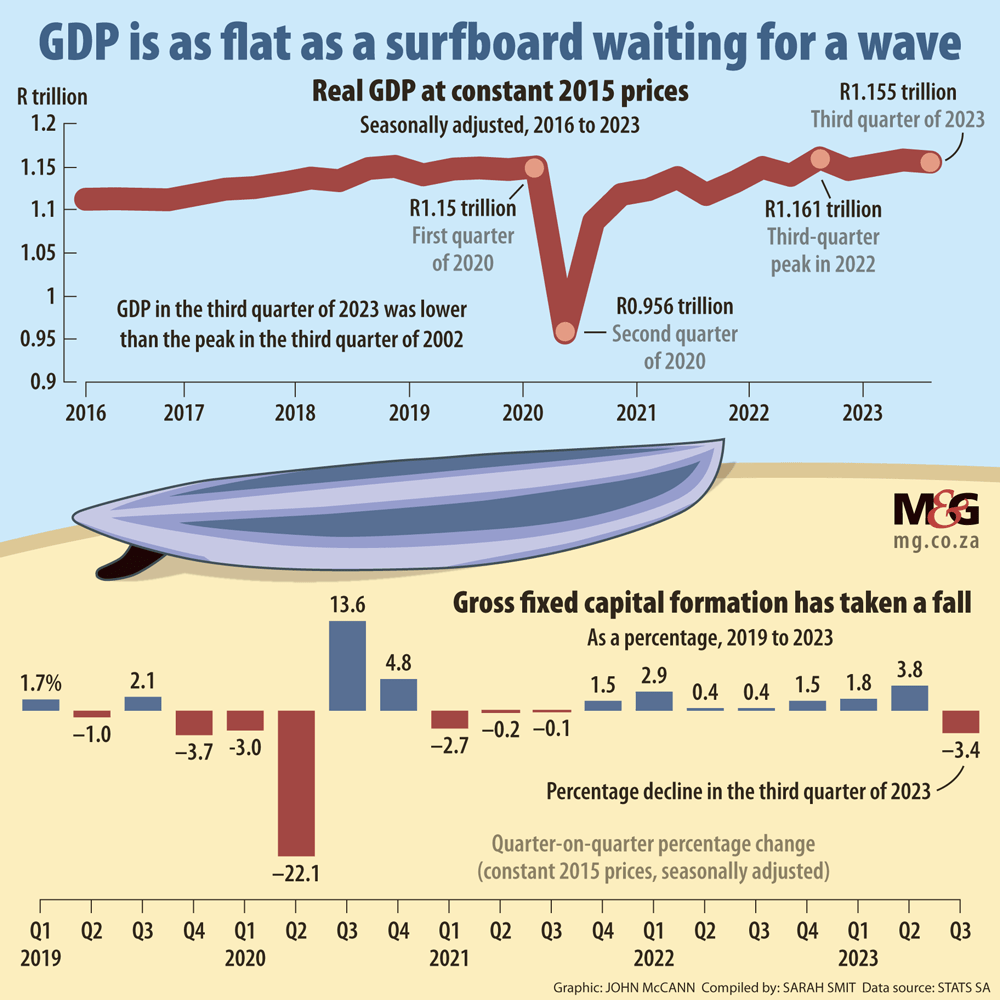

Earlier this week, data from Statistics South Africa painted another grim picture about the state of the country’s economy.

After declining 0.2% in the third quarter of the year, South Africa’s GDP is now only marginally bigger than it was prior to the pandemic. StatsSA cited persistent rotational load-shedding, logistical constraints, as well as the challenging global environment as reasons for the contraction.

While the economy saw contractions on the supply side — especially from the agriculture industry — there were also significant declines on the demand side, namely in household consumption and fixed investment, which fell 3.4% quarter-on-quarter.

Remarking on the GDP outcome, Nedbank noted that the outlook for the rest of the year and into the new year remains bleak. “Load-shedding has returned with a vengeance as Eskom resumed regular maintenance and emergency reserves dwindled. Logistical constraints have also intensified. Both will continue to amplify operating costs, erode profits, and weigh down activity,” the bank’s economists said in a research note.

Moreover, the economy has been hit by intensifying cyclical headwinds, such as tough financial conditions, slowing global demand for commodities and softer growth in China.

These problems, paired with the fact that households will continue to feel the strain of high interest rates, means companies will be reluctant to expand operations further, resulting in slower growth in fixed investment, according to Nedbank. The bank has forecast GDP growth of about 0.5% in 2023.

Despite being regarded as a business-friendly president when he was appointed, Ramaphosa’s first term hasn’t brought about the windfall of investment it promised. In fact, the president’s first three years also saw three consecutive contractions in gross fixed capital formation — the largest being in 2020, which marked the sharpest investment decline in at least two decades.

Investment has since recovered, albeit from a low base and not at a rate fast enough to spur large GDP and employment gains. Recent growth in capital formation has largely been attributed to increased renewable investments, unlocked in part thanks to Ramaphosa-era energy reforms.

Meanwhile, the prospect of a coalition disrupting the ANC’s hold on power has become more tangible than ever, with polls suggesting the governing party could slip below 50%. But a government without the ANC at the reins could prove a difficult sell to investors hoping for greater certainty in 2024.

After having proved its credentials during the pandemic response, organised business approached the president at the beginning of 2022 to express their concerns about the economy’s trajectory, according to Business for South Africa steering committee chair Martin Kingston.

“Before Covid we were going into a technical recession and getting downgraded. During Covid we were ravaged and the impact was felt everywhere in the economy — particularly among the youth, the unemployed and the most vulnerable. And as an economy we have recovered much more slowly than our peers … They have improved and we have flatlined,” Kingston noted.

At about this time, Ramaphosa announced in his State of the Nation address that social partners, including business, would be working on drafting a comprehensive social compact to grow the economy and address the country’s social challenges.

The compact would be finalised in 100 days, the president said.

Concerned that the social compact’s broad focus might create gridlocks, the private sector preferred a narrower focus, namely on energy, transport and logistics and crime and corruption where clear and tangible progress could be made and confidence rebuilt as quickly as possible.

“We wanted to ensure that the focus of our collaboration was achievable and addressed the most critical issues,” Kingston said.

“We engaged with the government for several months. We thought that we would need to focus on a much narrower and in a very deliberate way on a limited number of areas where we could collectively move the needle.”

The social compact never materialised. Instead, the private sector’s three-area focus became the genesis for the current joint effort by business and government.

(John McCann/M&G)

(John McCann/M&G)

But the partnership in its current form only really took off in early June this year.

According to Kingston, it has gained significant momentum, proving that business and government have found common ground.

Ramaphosa seems to concur. In a statement released last week to give an update on the collaboration, the president said: “Since we began, we have made significant progress in establishing structures and ways of working, mobilising resources and driving implementation of key actions. We see this partnership as evidence of the business community’s commitment to building our country and overcoming the challenges that we face.”

That said, there is no doubt that the private sector’s initial confidence in Ramaphosa has been knocked in recent years.

An index compiled by Rand Merchant Bank and the Bureau for Economic Research shows that, despite recovering after the 2020, business confidence has since reverted downwards.

“I think we are starting to make real progress. But is there some level of disappointment that it is slower and less impactful than it might have been to date? Yes. There is,” Kingston said.

“But I take a pragmatic view of that, looking at the things that we can do under the circumstances. We are working constructively with a democratically elected government. The electorate can vote differently next year, but in the meantime they are the government of the day and we are committed to working with them to ensure that we address critical challenges to achieve our potential.”

Early on in their collaboration with the government, organised business received some criticism for shoring up the ANC ahead of the election. In response business leaders have maintained their political neutrality.

Given the current predicament, the elections can’t come soon enough, former Goldman Sachs executive Colin Coleman said. “This question is, is anything going to change? Because the way I see it, the ANC government has provided no real leadership to pull the country in a particular direction.”

Coleman called the collaboration between the private sector and government the only real glimmer of hope. “But while that is one of the encouraging signs, it is not a strategy. And essentially, the government and its economic ministries are on autopilot — often in conflict with each other, within the same party, moving in different directions with contradictory policies,” he said.

Despite his administration’s failings, Coleman said no serious analyst expects Ramaphosa won’t end up serving another term.

Coleman noted that the overwhelming instinct within the business community is to do what they can to support the economy. “But at the end of the day, they will have to deal with the government of the day. And there is no alternative to dealing with the Ramaphosa administration, but they find it very frustrating,” he said.

This frustration lies in the feeling that Ramaphosa hasn’t effectively mobilised his administration to address the problems ailing the economy. “And some in the private sector would like to see an alternative political contender rise to the fore. But at this point in time, it’s a dangerous game for them.”