South Africa’s economy has bucked analysts’ modest expectations, recording a far more robust rebound than forecast.

Added to last week’s job figures — which showed that South Africa’s ultra-high unemployment rate had retreated for the third time in a row — the GDP data might be viewed as an encouraging turn in the country’s economic trajectory.

But economists are cautious about reading too much into the third-quarter rebound, citing the country’s ongoing energy crisis and the global downturn as major headwinds.

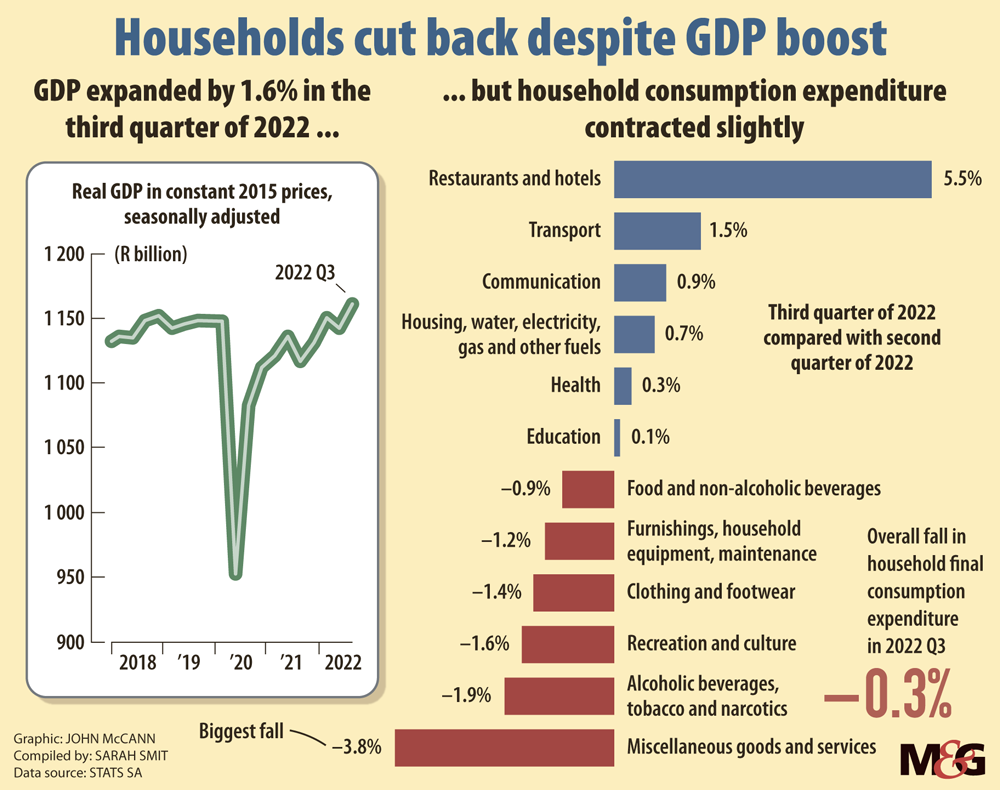

According to data released by Statistics South Africa on Tuesday, the country’s GDP expanded by 1.6% in the third quarter of 2022.

Third quarter growth means the size of the economy is now larger than it was before the onset of the Covid-19 pandemic in early 2020, suggesting that its recovery is now firmly back on track following the 0.7% contraction recorded the previous quarter.

Eight industries recorded positive growth between the second and third quarter of 2022, contributing to the rebound, which surprised on the upside.

Analysts were expecting far more modest growth of 0.4%.

Headwinds

But the more-spirited-than-expected rebound does not necessarily mean the economy has ended its go-slow, especially considering the third-quarter increase was largely driven by cyclical forces.

Sanisha Packirisamy, an economist at Momentum Investments, noted that the GDP figure got a boost from growth in inventories (which contributed 0.7 of a percentage point to the overall number) and net exports (which contributed one percentage point).

“We don’t believe either of these are sustainable, so I would caution against the strength of the third-quarter GDP number,” Packirisamy said.

“I would definitely suggest not reading too much into it. On the inventory side, we are pretty much back to pre-pandemic 2019 levels … Businesses are starting to accumulate inventory again, but I don’t expect them to get to the point where they are over-stocking to such an extent where they’re selling a massive amount of inventory. The demand is not there and so we think it’s a misallocation of capital by businesses.”

On exports, Packirisamy noted that a number of South Africa’s main trading partners — including China, the United Kingdom, the United States and Japan — will probably see softer growth in 2022 than previously expected.

In October, the International Monetary Fund forecast that global growth is forecast to slow from 6% in 2021 to 3.2% in 2022 and warned that the worst is yet to come.

This week, Fitch revised down its 2023 global growth forecast, citing the ratcheting-up of interest rates to tackle inflation as well as the deterioration of China’s property market.

The ratings agency now expects world gross domestic product to grow by 1.4% in 2023, revised down from 1.7% in its September global economic outlook.

It has cut its forecasts for the United States and China growth to 0.2% from 0.5% and to 4.1% from 4.5%, respectively.

Not environment for growth

Jee-A van der Linde, a senior economist at Oxford Economics, similarly cautioned against viewing the third-quarter rebound as a sign of the economy’s improved health.

The better GDP number means that forecasters will adjust their 2022 growth up to 2% or above, compared with previous expectation of about 1.8%. “But that doesn’t really address some of the underlying issues. Globally, we have growth slowing … Exports are a function of high commodity prices and that is changing.”

Both Packirisamy and Van der Linde flagged the marked decline in household final consumption expenditure, which decreased by 0.3% in the third quarter.

The decline in household expenditure was the biggest drag on the GDP number, contributing -0.2 of a percentage point to overall growth. During the previous three quarters, household consumption had added positively to the GDP number.

“In the first half of this year, it was quite evident that exports and households were driving the recovery,” Packirisamy said.

“And I think we saw a bit of a turning point in the third quarter, with household consumption detracting from the GDP number. We are starting to see the effect of higher food and fuel prices and weaker sentiment.”

Despite inflation having reached its expected peak in July, Van der Linde expects that households will continue to feel the pressure of high prices in the coming quarters.

“Costs will continue to remain sticky. And if you look at the monetary policy side, the South African Reserve Bank is not suddenly going to lower interest rates … So financial conditions are going to remain tight,” he said.

The South African economy, Van der Linde added, is still in recovery mode, compared to advanced economies which have recorded more robust rebounds.

“It has sort of been a stop-go for the domestic economy because of numerous factors. We had the floods in KwaZulu-Natal earlier this year and the riots and looting in mid-2021. At least from the supply side, the economy will still be recovering from those and then you have these sporadic power outages,” he said.

“It doesn’t really create the environment for growth.”

(John McCann/M&G)

(John McCann/M&G)

High base

Before the third quarter GDP release, forecasters had pencilled in very conservative growth in the fourth quarter.

In November, the South African Reserve Bank’s monetary policy committee, which also underestimated the third-quarter rebound, forecast that the economy would grow by a mere 0.1% in the fourth quarter due to the negative effect of load-shedding.

Now that fourth quarter growth will be calculated off of a higher base, that number may actually come out even lower. Load-shedding, as well as the closing down of industry over the festive season, could result in a negative fourth-quarter print.

The higher base for 2022 will also have a suppressing effect on growth forecasts for 2023 and 2024. Packirisamy’s earlier growth forecast for 2023 was at 1.4%. But a higher 2022 GDP number brings this number down closer to 1%.

Forecasts for South Africa’s GDP in upcoming years are already very low and the country’s low growth potential has been flagged by ratings agencies as a key credit weakness.

Low growth in coming years, as well as political pressures that will inevitably arise in the lead-up to the 2024 general elections, will threaten policy certainty and investor confidence going forward. If investment is constrained, growth will suffer.

Business confidence slipped slightly in the fourth quarter, according to an index compiled by the Bureau for Economic Research and Rand Merchant Bank (RMB). According to the index, more than six out of 10 respondents remained dissatisfied with prevailing business conditions.

Though the compilers of the index noted the presence of underlying resilience and recovery in certain sectors of the economy, RMB chief economist Ettienne le Roux said there is no denying the fact that the economy would be doing so much better were it not for the slow pace of government’s structural reforms.

“Going into next year,” Packirisamy said, “what is happening on the political scene is going to add to policy uncertainty. Already about three quarters of businesses are saying we are not investing because of policy uncertainty. This is just going to dampen the mood even further.”

[/membership]